The LVMH stock has given much pleasure to long-term investors. The shares of the only luxury goods company active in all the main markets of the luxury segment have achieved an average annual return of over 20 percent since 2009. Not even the COVID-19 shock could permanently affect the triumphant performance. Even though the share lost almost 30 percent in value parallel with the market, it is now back just below its all-time high of EUR 440. In this fundamental LVMH stock analysis, we check whether a purchase of the stock is still worthwhile or whether it seems more like a luxury object for enthusiasts. Also noteworthy is the Tiffany takeover that is threatened by failure and whether failure would be more of a setback or even a better scenario for shareholders.

An exclusive business: How LVMH generates money

LVMH (Moët Hennessy Louis Vuitton) is the largest luxury goods company in the world and was created in 1987 due to the merger of Louis Vuitton and Moët Hennessy. The individual companies themselves already had a long history. For example, the foundation of the champagne manufacturer Moët et Chandondes dates back to 1743. Today, the LVMH company is divided into six segments containing over 70 brands. These brands or houses, as the company calls them, operate largely independently, which gives them a high degree of flexibility. At the same time, however, they benefit from the parent company’s market research, distribution channels, and logistics networks.

The „Watches and Jewelry“ segment

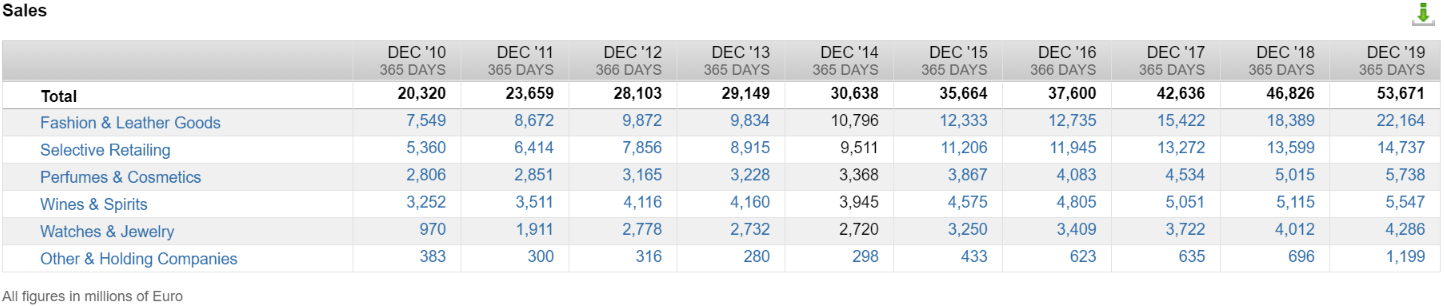

LVMH generates 8 percent of its revenue with the sale of jewelry and watches. LVMH has six brands in its portfolio, three from the watch segment, and three from the jewelry segment. The watch segment includes the brands Chaumet, TAG Heuer, and Zenith, while in the jewelry segment LVMH owns the brands Bulgari, Fred, and Hublot. In 2019 these six brands generated EUR 4.3 billion in revenue.

The „Wines and Spirits“ segment

In the wine and spirits segment, LVMH holds 23 brands, with which the company generated 10 percent of total sales in 2019 (EUR 5.5 billion). This segment includes luxury brands in wine, champagne, cognac, rum, vodka, and whiskey. Moët & Chandon, Dom Pérignon, Veuve Clicquot, Ardberg, and Hennessy are the most iconic brands. It is impressive that these brands are several hundred years old. The oldest winery in LVMH’s portfolio, Clos des Lambrays, was founded in 1365. It is impressive that these brands are several hundred years old. The oldest winery in LVMH’s portfolio, Clos des Lambrays, was founded in 1365.

The „Perfumes and Cosmetics“ segment

LVMH earns a further 13 percent of its revenue from perfume and cosmetics. 14 brands generated nearly EUR 7 billion in 2019, with cosmetics accounting for the lion’s share of 75 percent. Brands in the segment include Guerlain, Christian Dior, Givenchy, among others.

The „Fashion and Leather Goods“ segment

LVMH generates most of its revenue in the iconic fashion and leather goods segment. In 2019, 17 brands such as Louis Vuitton, Rimowa, and Loewe generated EUR 22.2 billion or 41 percent of total sales.

The „Selective Retailing“ and „Other Activities“ segments

In the “Selective Retailing” segment, LVMH distributes its products in a total of 2011 stores. These include duty-free stores or the boutiques of the LVMH company Starboard Cruise Services. With Starboard Cruise Services, LVMH meets the appetite of cruise ship passengers, which is currently out of fashion due to the corona pandemic. In an exclusive environment, passengers contributed EUR 14.7 billion to the segment’s total revenues in 2019 with their purchases.

LVMH is active in other markets through its small “Other Activities” segment. These include yachts (Royal Van Lent), media (Les Echos, Le Parisien), and hotels (Cheval Blanc Courchevel).

Why is LVMH so successful and what are its weak points?

All LVMH products have a touch of exclusivity. This exclusivity and the prestige that comes with it make ordinary, functional products like a bag a status symbol. LVMH does not build up these brands itself but buys them. Thus, in 2011 it acquired Bulgari. In 2016, LVMH bought an 80 stake in the luxury suitcase manufacturer Rimowa and in 2017, LVMH bought the fashion division of Dior. All these purchases save LVMH from having to build up a new brand. Instead, it “merely” has to maintain the brands it has purchased, some of which have a centuries-old prestige character.

To do this, LVMH resorts to the usual tricks of the trade: artificial scarcity and marketing, which probably sounds more comfortable than it is. After all, copy-cats and the so-called grey market threaten the prestige character of luxury goods and, in extreme cases, even force companies like LVMH to destroy their products or buy back goods from unlicensed dealers. Jean-Claude-Biver, head of LVMH’s Watch Division, summarizes the extent of the threat:

In luxury goods, when you break the illusion of prestige, the dream, the prices, it takes away the confidence. It means slow death for luxury goods.

This threat is, however, rather a problem affecting the entire luxury industry. In particular, LVMH has shown that it can maintain its products’ prestige and shortage of supply. This is ensured by CEO Bernard Arnauld, who, through his holding company, is LVMH’s largest shareholder with 47 percent and one of the five wealthiest people on earth. I like it when owners or even founding families run a company. That is no guarantee of success, but it is a good thing. However, as described in my previous Henkel analysis, there is a connection between family ownership and far-sighted management, where thinking is not in quarters but decades or generations.

Revenue growth with a crisis-typical slump

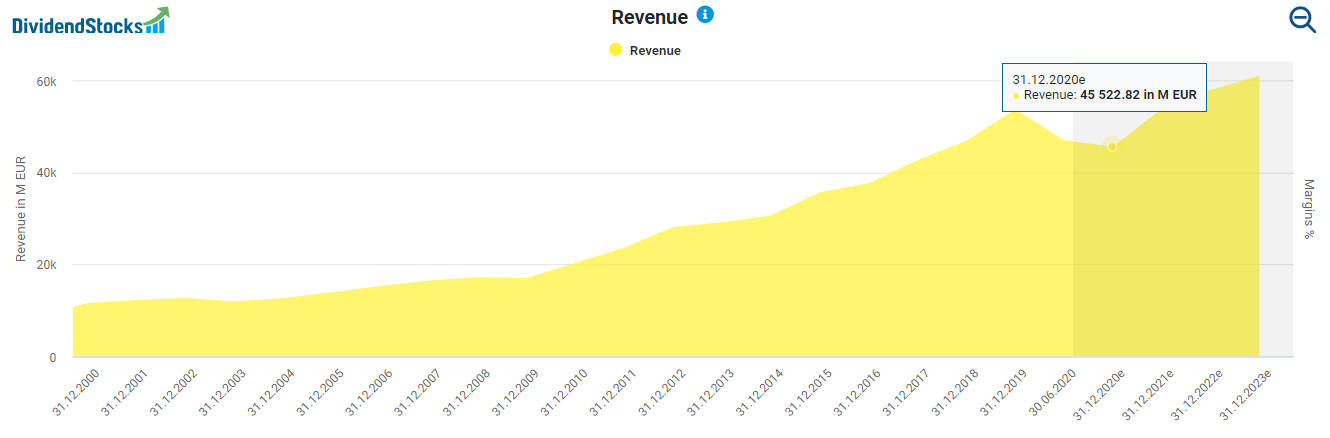

For decades, LVMH has benefited from a growing and luxury-seeking middle and upper class. The growth of the Asian markets, especially the Chinese market, and the already mentioned strategy of buying established brands contribute to this. Accordingly, sales have developed well over the last 30 years. From just EUR 3 billion in 1990 to EUR 53.7 billion in 2019, LVMH is also benefiting from its global footprint. In 2019, LVMH generated 37 percent of its revenues in Asia, followed by Europe (28 percent) and the USA (24 percent). This diversification ensures that currency fluctuations are smoothed out especially against the background of the currently weak US dollar and the strong euro.

However, the revenue performance, as shown at DividendStocks.Cash also shows that luxury goods are cyclical in nature and, therefore, only enjoy a boom in times of economic prosperity. Thus, revenue declined both in 2009 and during the Corona crisis. The decline in revenue this year was artificially exacerbated by the state-imposed store closures. Sales in the first six months of 2020 fell by a substantial 27 percent. According to the forecasts, however, next year, it is expected to exceed the previous year’s level again and continue to grow.

How profitable is LVMH

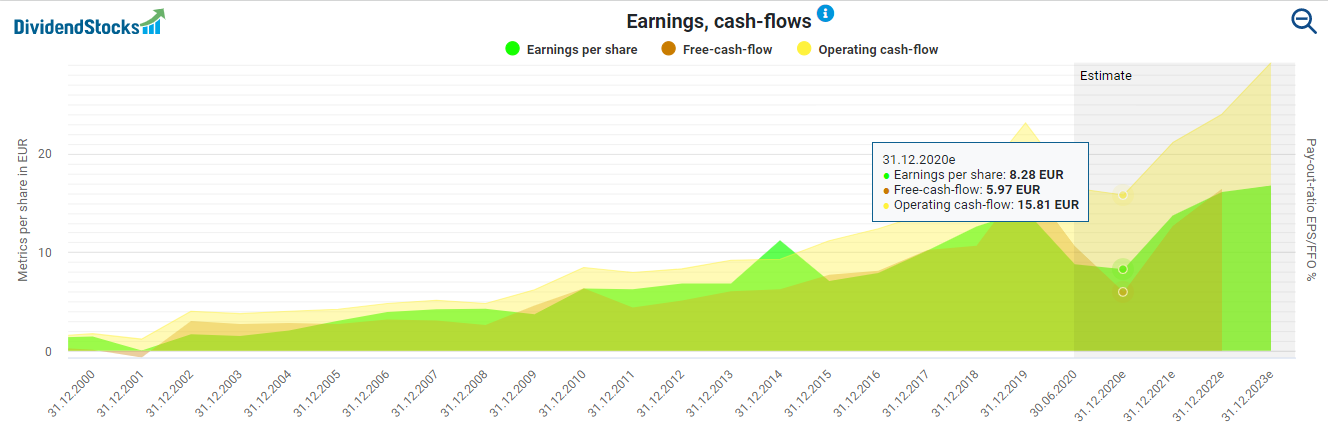

LVMH operates profitably and has not recorded one single year of losses in the past 30 years. From EUR 1.45 in 2000, LVMH increased earnings per share to EUR 14.23 last year. Cash flow from operating activities has also grown enormously, from EUR 1.18 per share in 2000 to EUR 23.13 per share in 2019. However, also the profitability shows the cyclical nature of the business. As a result of the corona crisis, profits collapsed by almost 70 percent in the first six months of 2020.

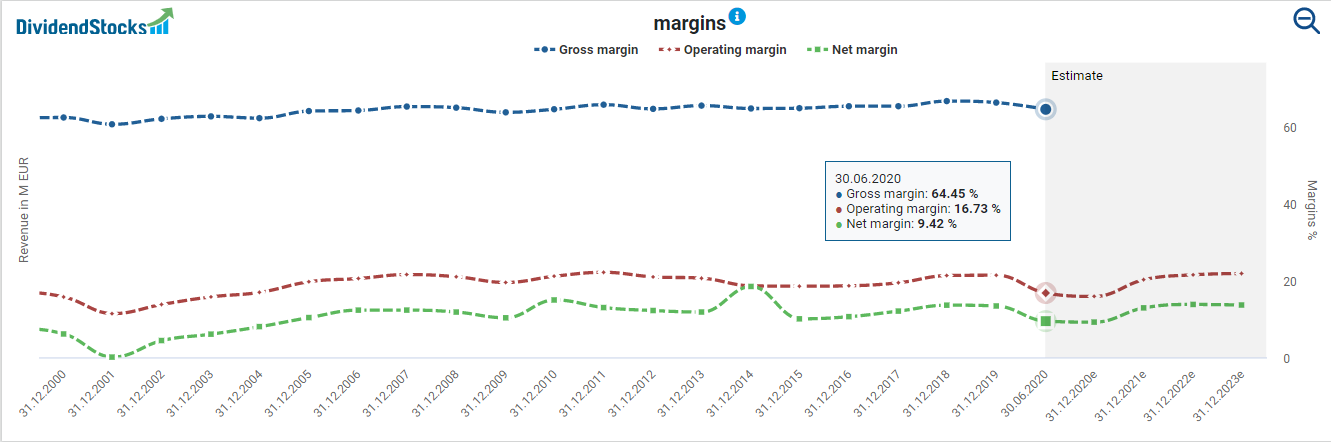

Accordingly, margins will decline in 2020, although their stability in recent years suggests that the overall profitability is assured. Nevertheless, the operating margin and net margin are relatively low, mainly due to high marketing expenses.

However, Hermes shows that better margins are achievable in the luxury goods sector. With a lower gross margin of 60 percent, competitor Hermes has a much higher operating margin of 29 percent and a net margin of 18 percent, which is twice as high.

Is the dividend of the LVMH stock safe?

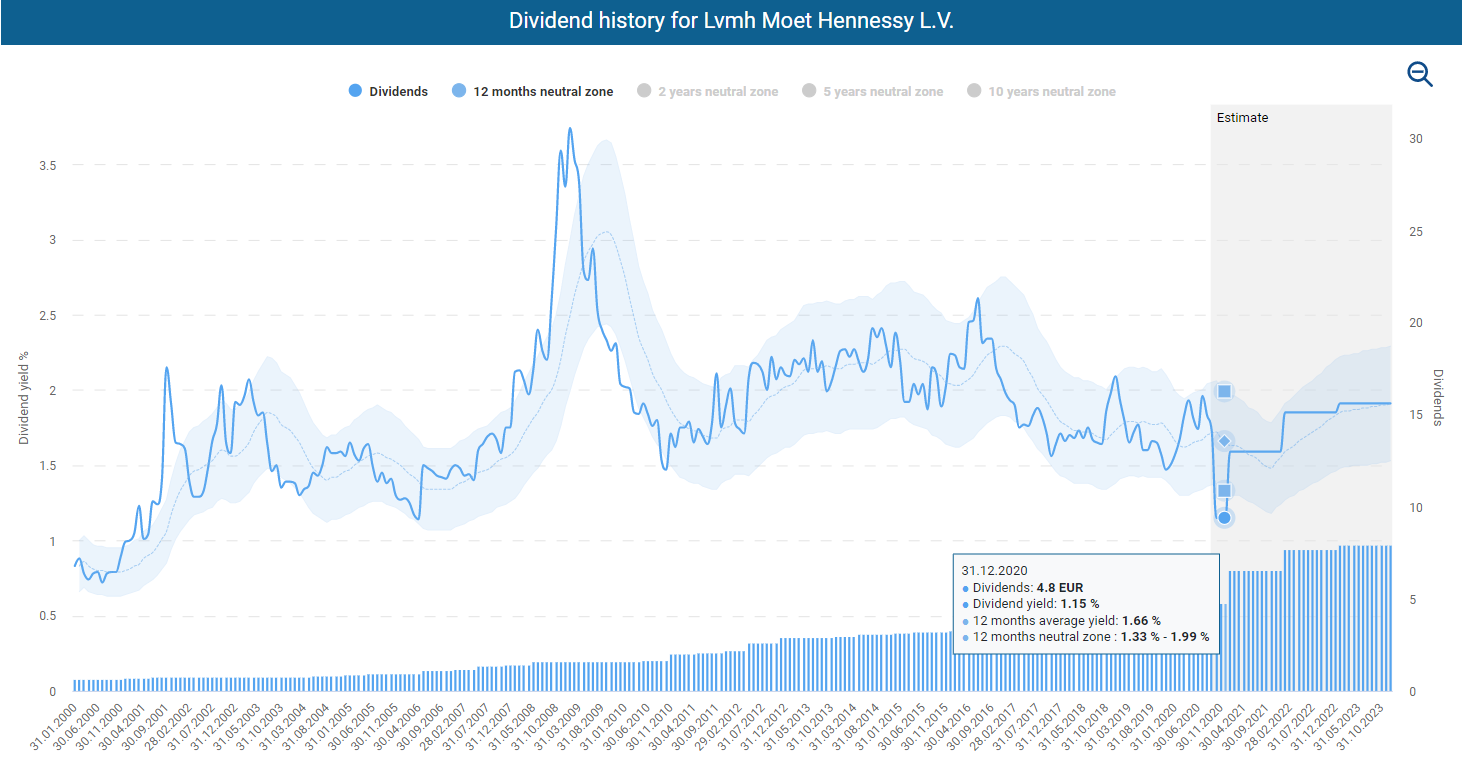

The LVMH share was a growth jewel for dividend chasers searching for a predictable passive income. Although the company only kept dividend payments stable at EUR 1.6 per share during the financial crisis of 2009, dividend fans have nevertheless come at their expense over the past decades. While LVMH increased its dividend from EUR 0.68 in 2000 to EUR 7.2 in 2019 with semiannual distributions, a bitter pill followed with the coronavirus.

Against the backdrop of uncertain developments and the massive slump in profits, the management cut the dividend by a third to EUR 4.8. The dividend yield has thus fallen to an even lower level of 1.1 percent. Even if we assume that payments will reach the old level by 2022 at the latest, the dividend yield would still be a meager 1.5% based on the current share price.

With a regular payout ratio of between 30 and 50 percent of profits and 40 and 55 percent of free cash flow before the coronavirus outbreak, the dividend was always within a safe range. However, extreme events, such as the corona crisis show that shareholders are never immune to unpleasant surprises.

The fair value calculation of the LVMH stock

What the price increases and the low dividend yield already indicate is confirmed by a look at the dynamic share valuation: The LVMH share is historically overvalued. The adjusted P/E ratio of 24, based on the 2019 earnings not affected by the coronavirus, also indicates a significant overvaluation. Based on the historical P/E ratio and price-to-cash flow ratio and considering last year’s profits and operating cash flow, the resulting fair share price indicates an overvaluation by more than 10 percent. Thus, even if we assume a rapid recovery of the business, the LVMH share would remain overvalued for the next three years.

Is a possible failure of the Tiffany acquisition good or bad for LVMH?

With the acquisition of Tiffany announced at the end of 2019 for USD 16.2 billion, LVMH wanted to strengthen its position in the jewelry sector and further expand its presence in the US. Allegedly, the French government asked LVMH to postpone the merger due to customs disputes with the US. From a fundamental point of view, a failure of the takeover should be bearable for shareholders. Although the prestige character fits well into LVMH’s portfolio, in the end, it would have been just the purchase of another brand. Even before the coronavirus emerged, the price for the 180-year-old jewelry company was too expensive in my view. The corona crisis has further intensified the overvaluation.

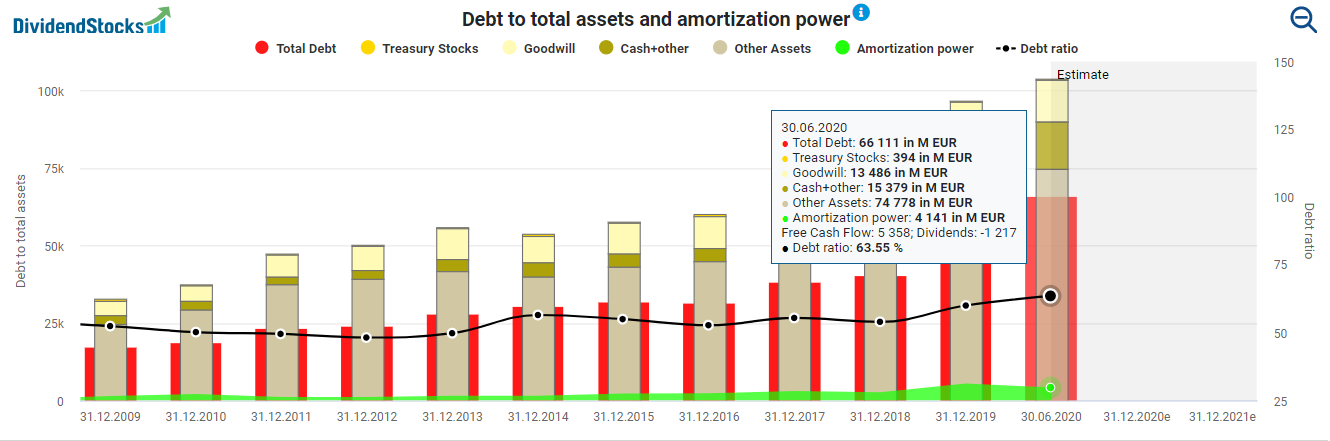

Therefore, Tiffany is excessively expensive and would also contribute little to an improvement in profitability. With a gross margin of 62.4 percent, an operating margin of 16.5 percent, and a net margin of 12.2 percent in 2019, it is somewhat on par with LVMH. Another advantage of the failure of the acquisition is that LVMH could lighten its balance sheet somewhat. The debt ratio is relatively high after rising from 53 percent to 63 percent in 2019. The ability to repay the debt, which is primarily based on cash flow, could decline significantly again depending on the further course of the corona crisis. Therefore, it is farsighted to keep the reins somewhat tighter.

Conclusion: LVMH stock – exclusivity has its price

With the LVMH stock, you get the global luxury boom into your portfolio. The company has an excellent position and should continue to profit from growth in essential markets in the long term. Unfortunately, several metrics indicate an overvaluation. The overvaluation even remains if we exclude the slump in the operating business caused by the coronavirus. For dividend hunters, the share also has its dark sides. Not only is the dividend yield historically low, but with its dividend cut, LVMH has also shown that the business remains cyclical. Because of the high current share price, the stock is not a buy for me, but rather a case for a long-term share savings plan.

Did you like the article? Stay tuned for the following content… It is all entirely for free! Enjoy!

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.