Welcome to a new report of my Dividend Diary on the TEV Blog. Here, I report the development of a cash flow-oriented investment approach that focuses on generating a passive income through dividends. Against this background, the goal is not to outperform the market but to put food on the table through a regular income via dividends.

With the Dividend Diary, I document how a cash-flow investment approach can be part of well-balanced wealth management. To keep things simple, I have built three pillars:

- Active income.

- Passive income.

- Conversion.

Dividends fall into the last two categories. They are passive because they provide a cash flow without me having to go to work. Additionally, they are an essential pillar for the conversion since they can be reinvested to generate even more income in the future. That is the Theory. Now let’s get down to practice.

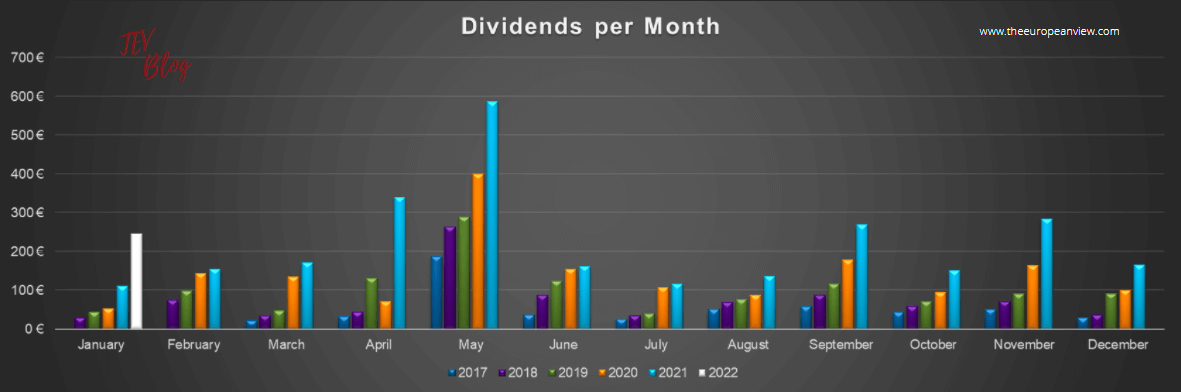

My monthly income through dividends in January:

This month, my cash-flow approach generated the following income through dividends:

- MSCI World Energy ETF (59.16 EUR)

- Automatic Data Processing (7.01 EUR)

- Kimberly-Clark (23.87 EUR)

- HP Inc. (13.98 EUR)

- Iron Mountain (15.29 EUR)

- Merck & Co. (18.09 EUR)

- PepsiCo Inc. (12.89 EUR)

- Altria (21.58 EUR)

- GlaxoSmithKline (19.52 EUR)

- Leggett & Platt (20.03 EUR)

- Realty Income (6.97 EUR)

- Cisco (11.34 EUR)

- Campbell Soup (15.36 EUR).

The total monthly income through dividends in January (after taxes) was: € 245.09 /appr. $ 273

Dividend income report check

The start of the new year was very successful. My income from dividends of almost € 250 was more than twice as high as in the previous year. Things can continue like this. Especially given all the noise and volatility on the stock markets, it feels very good to see how reliably, calmly, and smoothly the dividend income comes in every month. It almost has something mediative compared to all the noise and chatter on the social media platforms. Below you can see an overview of the long-term development of my monthly cash flows.

Success lies in calmness and long-term thinking

The great development has several reasons. First and foremost, I stay out of the bubbles or bubble-like asset classes in general. By following that approach, I invest in rationally valued stocks. Within that asset class, I try to avoid hype stocks. And thirdly, I also don’t change my strategy every few months. I started investing purposefully in dividend stocks in my mid-20s. Before that, I invested rather randomly here and there, traded gold mines and ETFs with c1ertificates. Yep, I was an idiot.

Now, I’m in my early 30s. And it seems that I found my strategy. Plus, I have many more years to learn, and I look forward to growing my garden of sweet, fruity dividends even further. Having that said, I wouldn’t mind if the stock markets take another walk south 🙂 . But who knows whether the stock markets will do us this favor. Some say that a crash is imminent. They point to a possible shift in the interest rate environment. However, history shows that there are always two ways to read the stock markets, and I think it’s quite possible that prices will continue to go up over the next few months despite a turnaround in interest rates. Therefore, I try to avoid panic and remain optimistic.

Stocks I sold in January

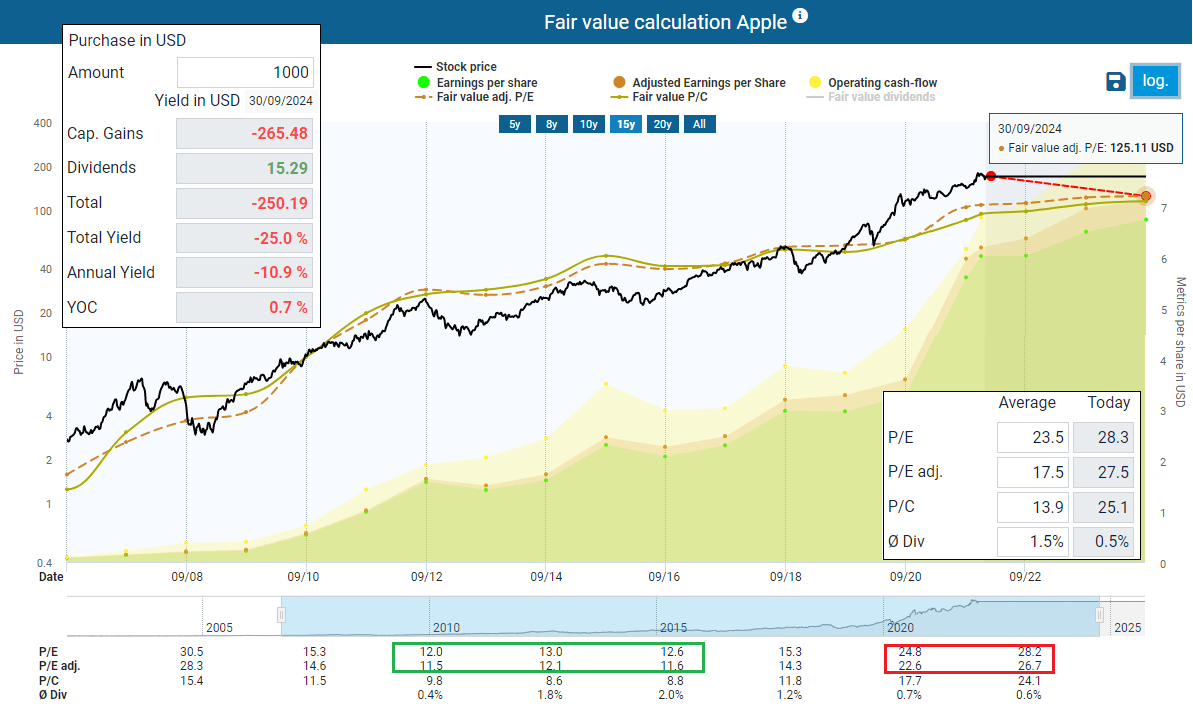

I sold 10 shares of my Apple holding in early January.

Apple is an excellent company but overvalued

To make things pretty clear right from the beginning: Apple is an excellent company, but the stock is simply overvalued. When I bought my Apple shares, the sentiment was totally different. Back then, the stock was not a hype stock and had just a P/E ratio between 11 and 13. Many investors were afraid that the growth with iPhones would reach the limits.

iPhone dominance is undoubtedly a luxury problem but also a risk for investors

From today’s perspective, the valuation at that time was absurdly cheap. But that’s the kind of thing that shows how investors’ views can change. If you look closely, you will see that iPhones are still Apple’s most important business. That hasn’t changed much in recent years, despite growth in its other businesses. The dependency has decreased somewhat but is still very high at over 50 percent.

| FY15 | FY16 | FY17 | FY18 | FY19 | FY20 | FY21 | |

| Total (in Mio. USD) | 233,715 | 215,639 | 229,234 | 265,595 | 260,174 | 274,515 | 365,817 |

| iPhone | 155,041 (66.3%) | 136,700 (63.4%) | 141,319 (61.6%) | 166,699 (62.8%) | 142,381 (54.7%) | 137,781 (50.2%) | 191,973 (52.5%) |

| Services | 19,909 (8.5%) | 24,348 (11.3%) | 29,980 (13.1%) | 37,190 (14%) | 46,291 (17.8%) | 53,768 (19.6%) | 68,425 (18.7%) |

| Wearables, Home and Accessories | 10,067 (4.3%) | 11,132 (5.2%) | 12,863 (5.6%) | 17,417 (6.6%) | 24,482 (9.4%) | 30,620 (11.2%) | 38,367 (10.5%) |

| Mac | 25,471 (10.9%) | 22,831 (10.6%) | 25,850 (11.3%) | 25,484 (9.6%) | 25,740 (9.9%) | 28,622 (10.4%) | 35,190 (9.6%) |

| iPad | 23,227 (9.9%) | 20,628 (9.6%) | 19,222 (8.4%) | 18,805 (7.1%) | 21,280 (8.2%) | 23,724 (8.6%) | 31,862 (8.7%) |

Sales in Mio. USD. In parentheses, the segment’s percentage revenue share of total revenue is shown.

After all, the other business units are also experiencing massive growth. Furthermore, the share of iPhone sales has only remained relatively stable because iPhone sales have also increased massively. Well, the iPhone dominance is undoubtedly a luxury problem for Apple. And fair enough, you can’t blame Apple for this success. Nevertheless, there is also no denying that Apple, with its 3 trillion market capitalization, is still vulnerable when saturation effects occur in the market. At the very least, it is enough to stir up old fears.

In addition, just take a look at the fundamentals stated further above. The increase in the P/E ratio impressively shows that the share has risen faster than the underlying business. Investors often make the mistake of viewing the share price and the operating business independently. Yet, it is a banal reality that the share price and the business are connected like a rubber band. The further the two are pulled apart, the more they snap back.

Conclusion: Taking some chips off the table and letting the rest grow

I am well aware that investors can make stocks fall from the sky quickly. I’ve been there and I’ve done that. Accordingly, I would never consider Apple as a defensive investment at current prices. Always remember that a stock that is rising twice as fast as the underlying business cannot be defensive.

That’s why, on such rare occasions, I sell parts of my holdings to create some liquidity for other stocks with lower valuations and higher dividend yields, i.e. higher monthly cash flow. At the same time, I diversify my portfolio and increase my monthly income. So by selling a bit, I am not trying to time the market. It is quite possible that the shares will continue to rise. I don’t care. For me, it’s about creating liquidity and taking some of the risks out of my holdings. With regard to my other Apple shares, I will hold on to them and won’t touch them.

Stock purchases in January

In January, I bought more shares of great companies so that the monthly income through dividends will continue to rise in the future.

- BASF (15 shares)

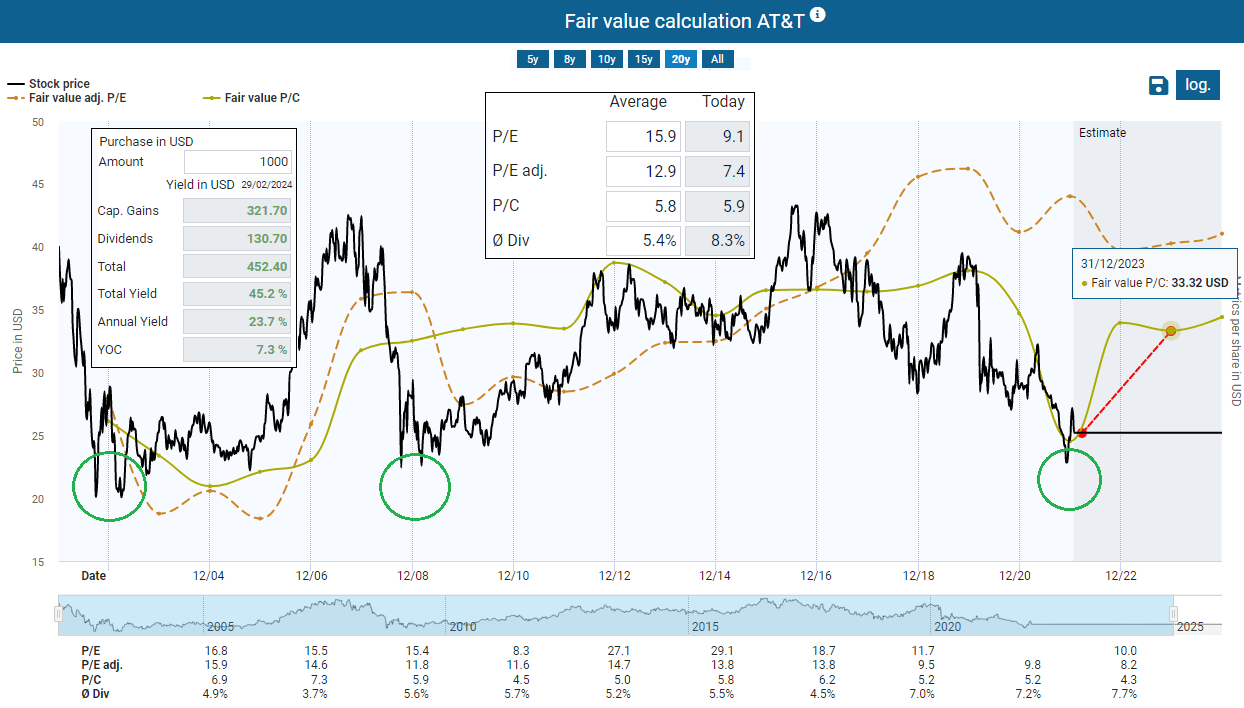

- AT&T (45 shares)

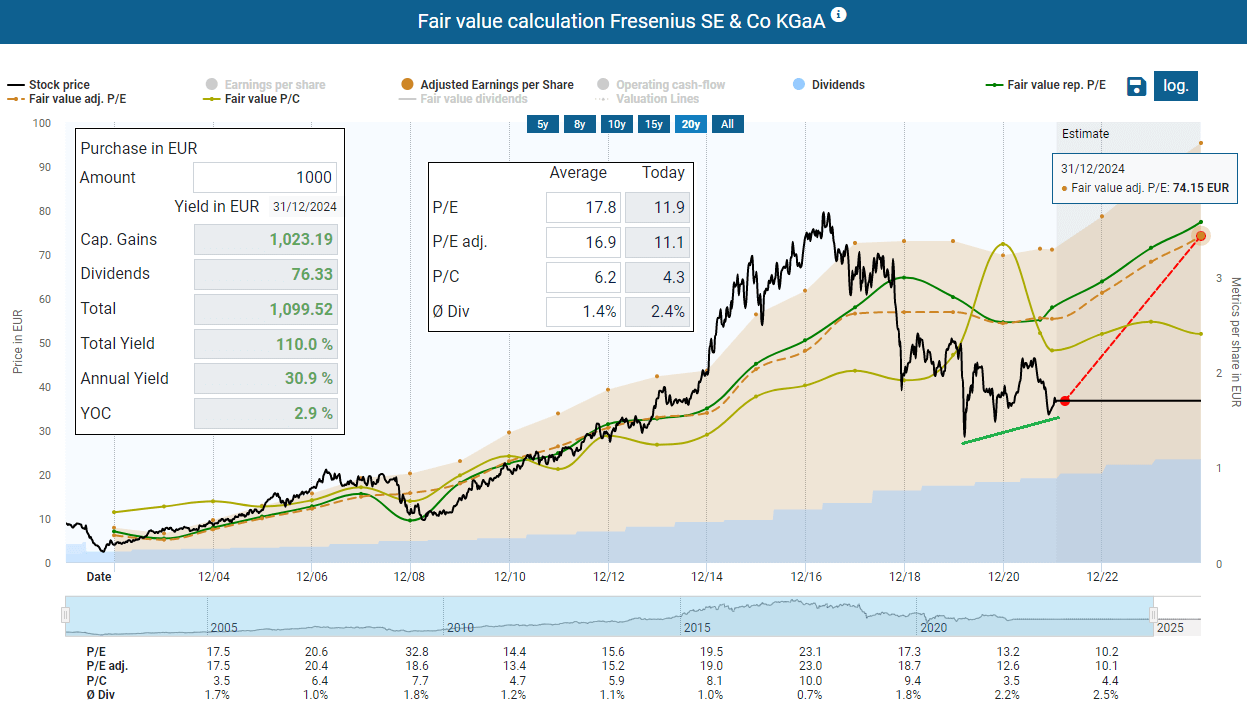

- Fresenius (25 shares)

- SAP (18 shares)

- Siemens (5 shares)

In the following, I will briefly explain why I bought these companies. Please do not expect a fundamental analysis. I will only mention some aspects per company that might be of interest to the readers. Maybe you will find inspiration for your investment. In case you disagree, feel free to write your opinion about my purchases in the comments.

Please keep in mind that this is only a non-representative sample of my overall asset management.

My last purchase of BASF shares was in September when I bought 30 shares. Since then, not much has changed and yet the share price fell at the beginning of January. I took advantage of this opportunity and bought more shares. At the same time, BASF decided for the first time in 13 years to launch a share buyback program with a volume of up to EUR 3 billion. Under this program, BASF intends to buy back its own shares in the period from January 11, 2022, to December 31, 2023. At the market price, the planned buyback program corresponds to a good five percent of the company’s market cap.

For me, this is a good sign of the company’s financial health. In addition, the BASF share is very fairly valued with an adjusted P/E ratio of just 10. The dividend yield of almost 5 percent is also extremely attractive. At these prices, I will therefore gladly continue to buy BASF.

AT&T is really crazy. In my opinion, management is doing more wrong than right. Most recently, the CEO caused confusion and wondered aloud whether the management should spin off WarnerMedia or split it off. The colleagues from Barron’s have summarized the different scenarios and their impacts in a good article:

A spinoff would be straightforward. AT&T would distribute an estimated 1.7 billion shares of the merged company to its shareholders, who would get nearly 0.25 share of Warner Brothers Discovery for each AT&T share. Such a move would be worth about $7 per AT&T share based on Discovery’s recent price of $30. Discovery stock is up over 20% in 2022, making it one the top stocks in the S&P 500.

The other option—a split-off—is more complicated. AT&T would offer holders the option of swapping their AT&T stock for Warner Brothers Discovery stock. To entice conversion, AT&T would likely offer its investors a bonus, with UBS analyst John Hodulik suggesting a deal of one share for one share.

It’s pretty hard to imagine but it looks like AT&T’s management thought about the structure of a deal after announcing the deal. Fortunately, in my view, AT&T is a company that could be run by idiots without going insolvent. With that, I’m not saying that the people around the new CEO John T. Stankey are idiots, but so far they have not managed to really increase the value of the company in the interest of the shareholders. But I have hope that after all the turmoil around WarnerMedia, calm will come. In addition, when I look at the big picture, AT&T is currently extremely attractively valued even despite a hefty potential dividend cut of 20-25 percent. In my view, a company with that fundamental valuation and a rather defensive business model deserves a place in a broadly diversified portfolio.

In addition, AT&T’s market capitalization of $180 billion includes WarnerMedia with all its well-known assets and services. Just for comparison: Netflix currently has a market capitalization of $170 billion. And even though I think the management of Netflix is much more capable and the comparison with WarnerMedia does not fit one hundred percent, WarnerMedia is not sufficiently represented in AT&T’s share price in my view. Accordingly, the divestiture (regardless of its structure) is likely to unlock value for shareholders.

Update: Now we have clarity

There’s never a dull moment at AT&T. At the beginning of February, only one week after the spin-off/split-off discussion, management has confirmed that there will be a spin-off. Here are the details:

- AT&T will receive $43 billion (subject to working capital and other adjustments) in a combination of cash and other consideration. The company will use this money to deleverage. By end of 2023, the company expects a Net Debt to adjusted EBITDA ratio of about 2.5x.

- AT&T’s shareholders will receive stock representing approximately 71 percent.

- Thus, AT&T shareholder can keep their shares and will receive on a tax-free basis for each AT&T share 0.24 shares of the new company, Warner Bros. Discovery.

- No action is required by AT&T’s shareholders to receive shares of WBD common stock in the merger when it occurs.

- Furthermore, AT&T also announced that it will pay an annual dividend of $1.11 per share following the close of the deal, down from $2.08 per share. That would indicate a payout ratio of about 40 percent.

Well, the good thing here is that investors have clarity. However, the dividend cut is a bit higher than expected (check for example Seeking Alpha articles that indicated a slightly higher dividend per share). However, I will not take action for the time being, even though I can well imagine that the share price will continue to fall, although a drastic dividend cut was clear (the market is irrational sometimes). With regard to the new company, I will treat the shares as a special dividend and then decide what to do with them.

I have described the company in a little more detail in another article (click here). The purchase served to increase my existing holding. The share is currently very favorably valued. Also, it could be that the stock has just entered a new uptrend. Admittedly, this perspective is still very shaky, but at some point, investors will have to buy if they want to increase their holdings. Time in the market is more important than timing the market.

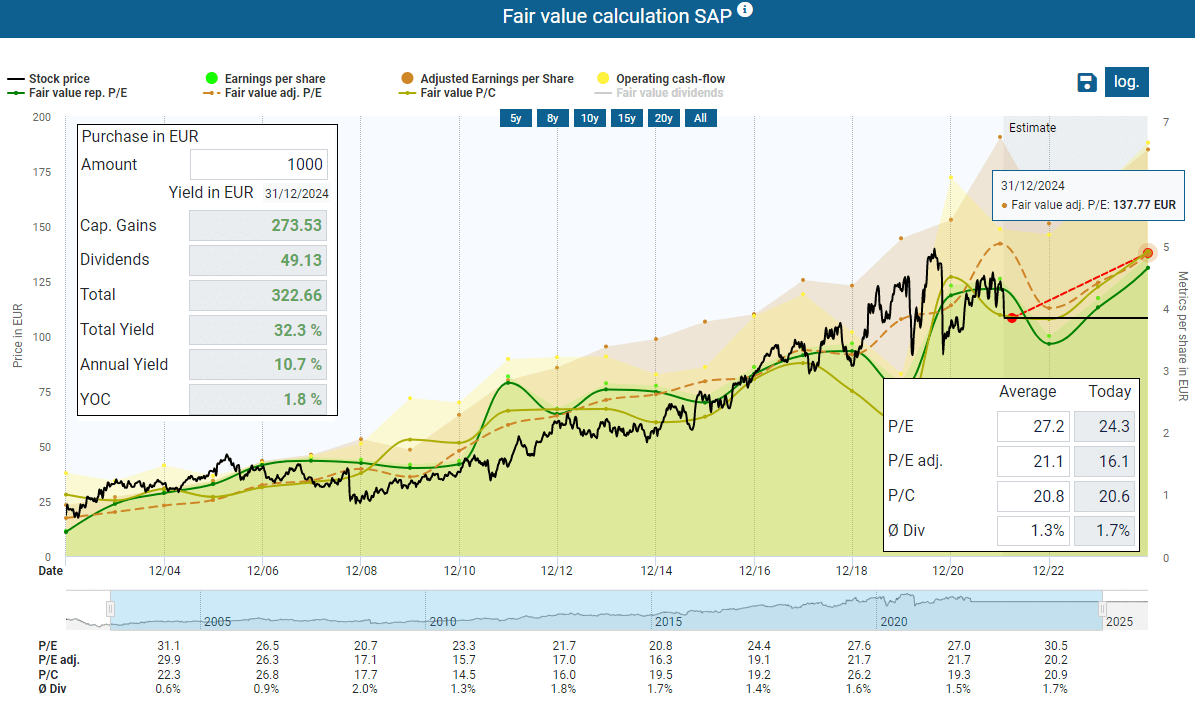

SAP has been on my watchlist for a long time, but somehow I always missed the entry. Finally, I have taken advantage of the recent correction and added 18 shares to my portfolio. Admittedly, the price-performance looks rather risky and somewhat like a shoulder-head-shoulder-formation. However, with 18 shares I am far from overweighting this position and can buy additional shares in the event of a further correction. Fundamentally, SAP is not too expensive. An adjusted P/E of 16 is acceptable for a tech stock (with some growth difficulties). Analysts also expect the company to increase earnings somewhat in the next few years.

If SAP manages its transformation to more cloud-based services, the current prices should be good buying opportunities. The market still has doubts. In addition, the sentiment currently speaks against tech stocks. So, in itself, a good time to go bargain hunting.

As a small footnote, SAP wants to acquire a majority stake in the financial platform Taulia and integrate it as an independent company. Taulia specializes in working capital management software.

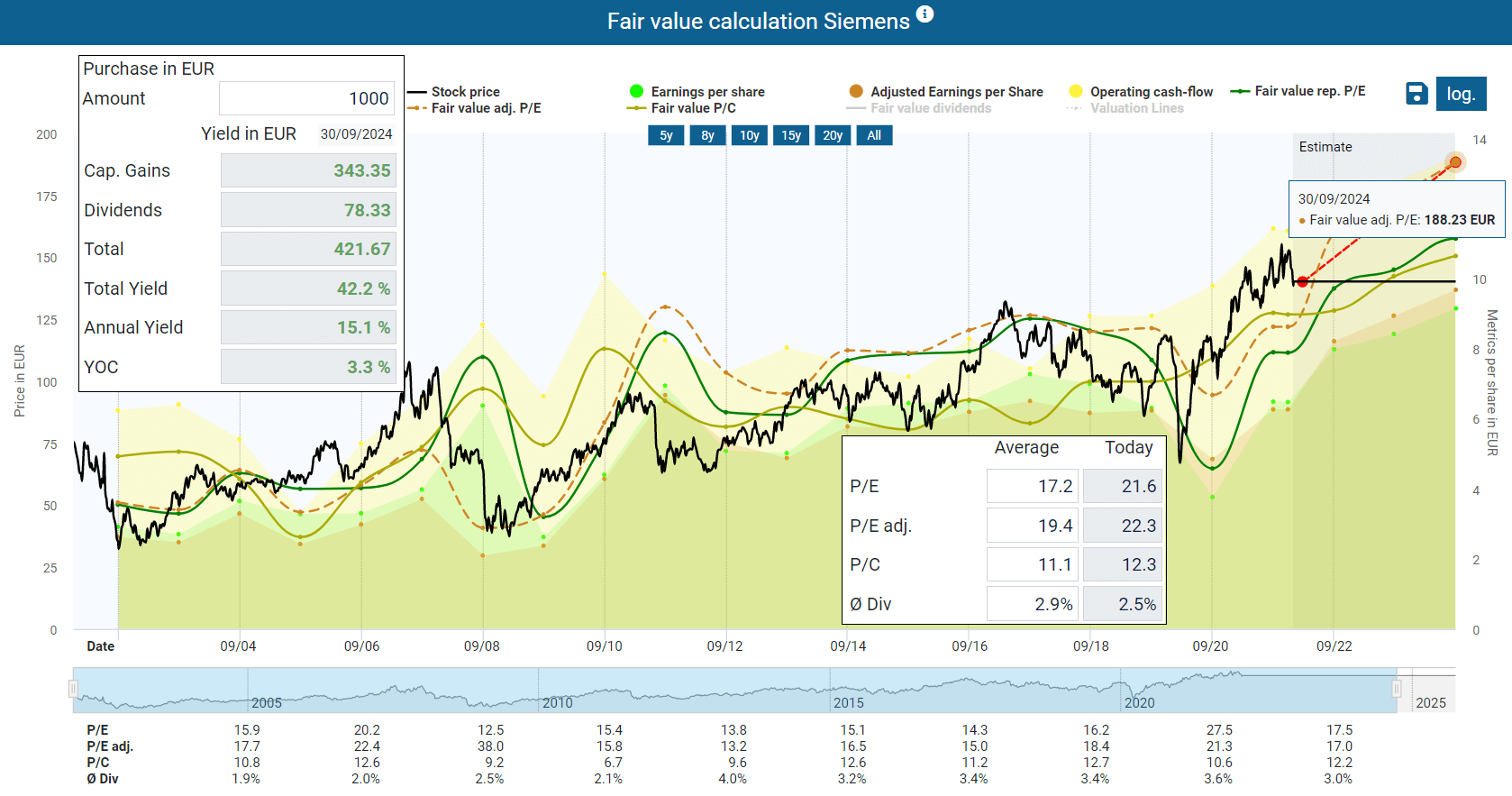

I chased so many post-buy opportunities in Siemens and ultimately never pressed the buy button that I have now increased my existing position somewhat. It was more of a spontaneous buy. But I am very happy with the management and the direction of the company. I’m bothered by the somewhat high valuation. But the analysts believe that the company will increase profits and sales in the next few years considerably, creating a decent upside potential. Let time tell if the purchase was wrong or right.

Watchlist for February

There will be some additional share purchases next month. As you may know, I am relatively flexible when it comes to new investments. Either I buy new positions, or I increase my shares in existing investments.

The following companies are on my watchlist in particular:

- Microsoft (MSFT)

- Digital Turbine (APPS)

- Johnson Outdoors (JOUT)

- Emerging Markets/Energy stocks/US Financials

- Unilever (UL)

- General Mills (GIS)

If you look at my report from last month, you will likely see that none of the companies I bought were on my watchlist. Why is that? Is the watchlist nonsense, and in the end, I only do what I want anyway? Yeah, a little bit. I don’t have a fixed system for my stock purchases, and that’s one thing I have to consider changing.

However, I have an extensive overview of many companies that I look at from time to time. The watchlist contains primarily companies that I have examined particularly carefully, where substantial changes are imminent or companies that are in my focus for other reasons.

These companies are present to me in some form, which is why I put them on the list and perhaps monitor them a little more closely than other companies. But it often happens that I invest in different companies when it seems convenient at that moment.