Welcome to a new report of my Dividend Diary on the TEV Blog. Here, I report the development of a cash flow-oriented investment approach that focuses on generating a passive income through dividends. Against this background, the goal is not to outperform the market but to put food on the table through a regular income via dividends.

With the Dividend Diary, I document how a cash-flow investment approach can be part of well-balanced wealth management. To keep things simple, I have built three pillars:

- Active income.

- Passive income.

- Conversion.

Dividends fall into the last two categories. They are passive because they provide a cash flow without me having to go to work. Additionally, they are an essential pillar for the conversion since they can be reinvested to generate even more income in the future. That is the Theory. Now let’s get down to practice.

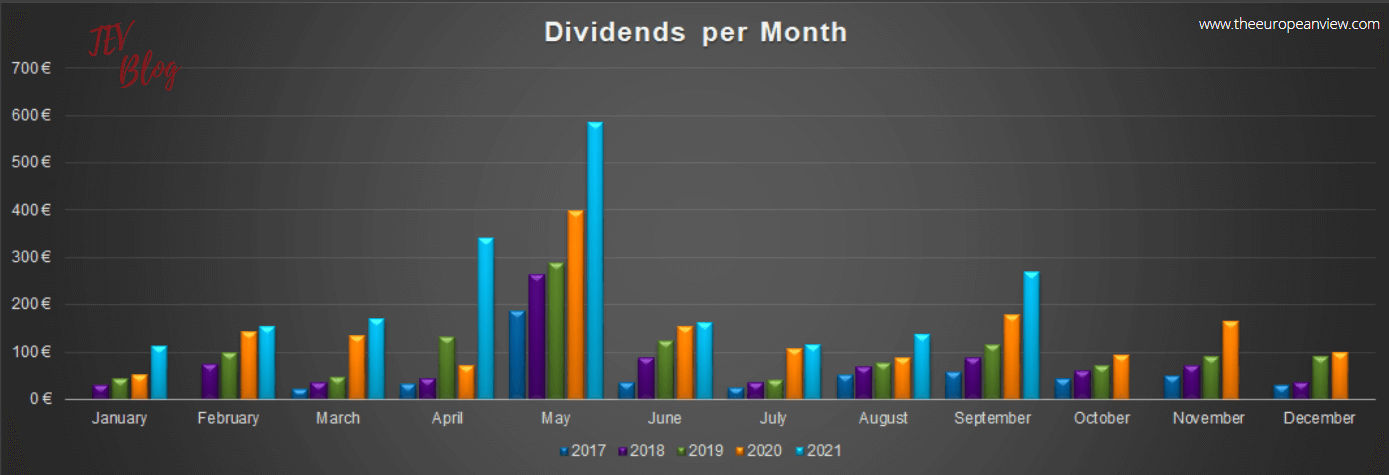

My monthly dividend income in September:

This month, my cash-flow approach generated the following income through dividends:

- Johnson & Johnson (13.24 EUR)

- Pfizer (16.30 EUR)

- Archer Daniels Midland (8.09 EUR)

- Unilever (14.54 EUR)

- Stroeer (33.87 EUR)

- IBM (15.43 EUR)

- Snap-on (9.25 EUR)

- 3M (12.06 EUR)

- Reckitt Benckiser Group (27.01 EUR)

- Realty Income (3.11 EUR)

- Royal Dutch Shell (9.48 EUR)

- Kontoor Brands (5.05 EUR)

- V.F. Corp (13.57 EUR)

- Logitech (46,53 EUR)

- Imperial Brands PLC (4.53 EUR)

- Broadcom (11.42 EUR)

- PepsiCo (10.92 EUR)

- Simon Property Group (5.72 EUR)

- Qualcomm (9.44 EUR)

The total income through dividends in September (after taxes) was: EUR 269.56 /appr. 312 USD

Dividend report check

September was better than I had expected. Compared to the previous year’s figure, cash flow from dividends increased by 50 percent. I have somewhat underestimated the number of my September payers. In addition, my regular re-purchases of shares lead to an increase in the monthly distribution. So I am still on track to double my monthly cash flow every two years. The overall development looks like this:

In the coming months, I expect to continue to exceed the previous year’s figures. The high increase in the value of the EUR last year should no longer have a distorting effect. In addition, my investments will surely provide one or the other cash flow increase. Two of my ETF holdings (see below) distribute their dividends in November and December, so there will be another sharp rise here.

Stocks I sold in September

I sold no shares this month.

Stock purchases in September

In September, I bought more shares of great companies so that the dividends will continue to rise in the future. All purchases were expansions of existing holdings. So no new companies entered my portfolio.

- Emerging Markets ETF (19 shares)

- Campbell Soup (55 shares)

- BASF (30 shares)

- 3M (7 shares)

In the following, I will briefly explain why I bought these companies. Please do not expect a fundamental analysis. I will only mention some aspects per company that might be of interest to the readers. Maybe you will find inspiration for your investment. In case you disagree, feel free to write your opinion about my purchases in the comments.

Please keep in mind that this is only a non-representative sample of my overall asset management.

In September, I increased my holdings in emerging market companies. As always, I used my existing Amundi ETF that distributes dividends in November. My last purchases were in September 2020, November 2020, December 2020, April 2021, June 2021, and August 2021.

The reasons for the purchase are the same as in the previous months – which is why I am refraining from great explanations and repetitions here. If there is no further slump in the coming weeks/months, this will probably be my last purchase for the time being. However, I do not rule out a spontaneous purchase. My exposure so far allows me some leeway and additional purchases. However, I don’t want to burn everything at once and think it would be good to wait a few months first.

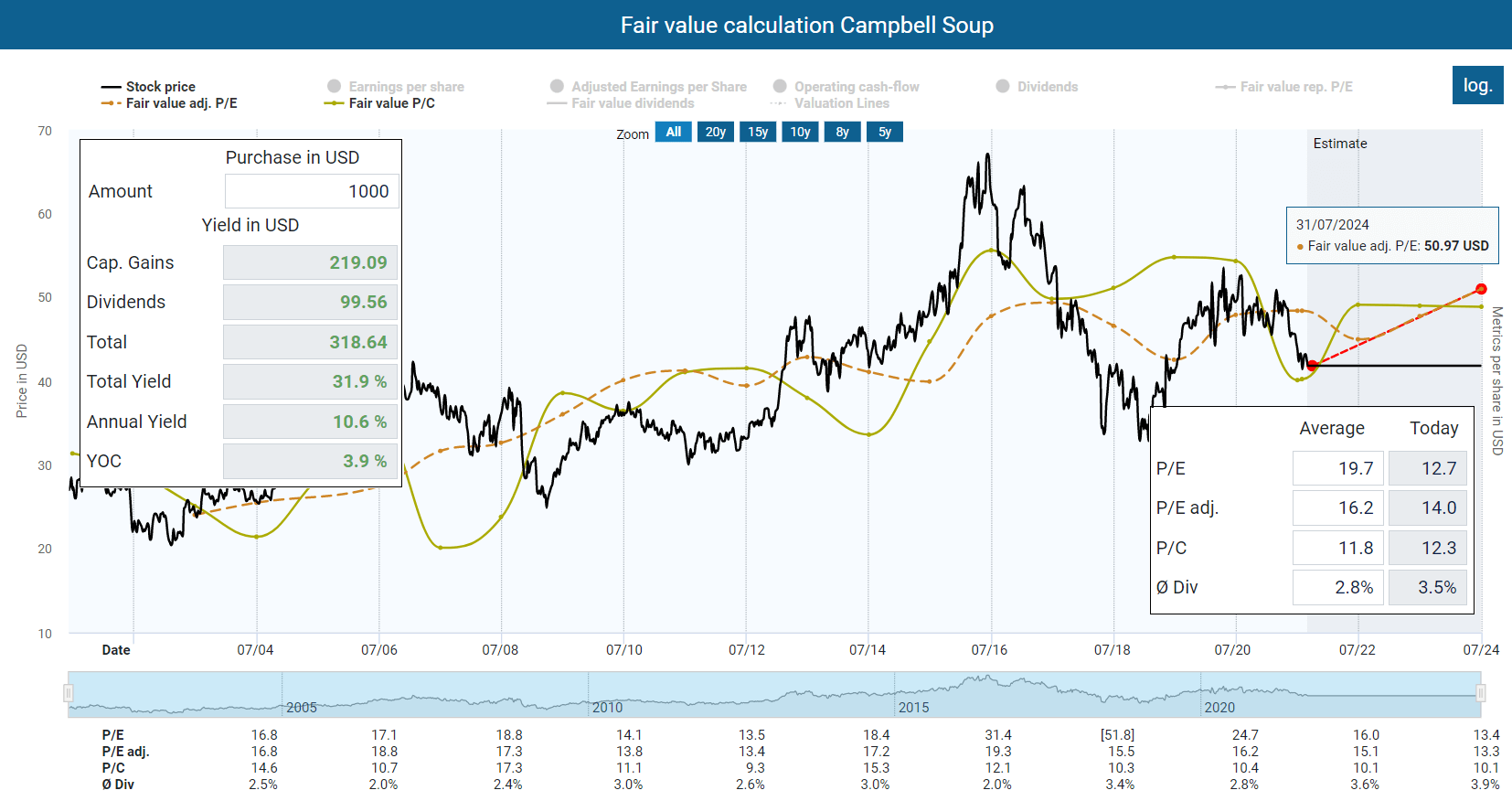

A spontaneous purchase was Campbell Soup. The company had been on my extended watchlist for a long time. The company produces and sells ready-made meals such as soups, simple meals, snacks, and drinks.

The share price performance was horrible. Since the all-time high of 2016, the share has lost more than 37 percent. The reason was mismanagement. Unwise transactions have inflated the balance sheet and have not led to the desired growth. Recently, however, the company has attracted attention with somewhat positive news.

Thus, the company was able to beat expectations. Compared to 2019, turnover rose by 9 percent in the last quarter. Although inflation is also weighing on the company, the management has been quite optimistic here. In addition, the company plans to launch a $500 million share buyback program funded by the company’s cash flow. Adjusted EPS increased 14 percent compared to Q4 2019, helping Campbell Soup grow in all quarters based on 2019 numbers. For the full year, the 2-year growth was 3 percent. For more insights, I recommend studying the presentation on the Q4 & Full Year Fiscal 2021 figures.

I like the company’s rather timeless core business and think that there is a lot of value if the proper management is running the business. Currently, the focus is on using the momentum and further sharpening the portfolio. This seems to be working. In the last quarter, 75 percent of the brand portfolio could maintain or gain market share. In addition, the company was able to work strongly on its balance sheet. The debt ratio measured by interest-bearing debt was 63 percent in 2018. Today it is “only” 41 percent. That is still high, but a significant improvement. The only remaining nuisance is the high goodwill of almost $4 billion. Further write-offs lurk here.

The next few years remain challenging, especially with pressure from continued cost price inflation. Growth will remain flat for the time being. However, I hope to see a more substantial improvement in growth momentum from 2023/2024 onwards. With this expectation, the share is currently highly cheap. The adjusted P/E ratio is only 14. Historically, the average value is 16.2. The current dividend yield of 3.5 percent is also tempting. The payout ratio is below 60 percent in terms of both cash and earnings. Measured against the expected results of the next few years, there is substantial upside potential. We will see if it materializes, but all in all, the share seemed to me to be a sound investment.

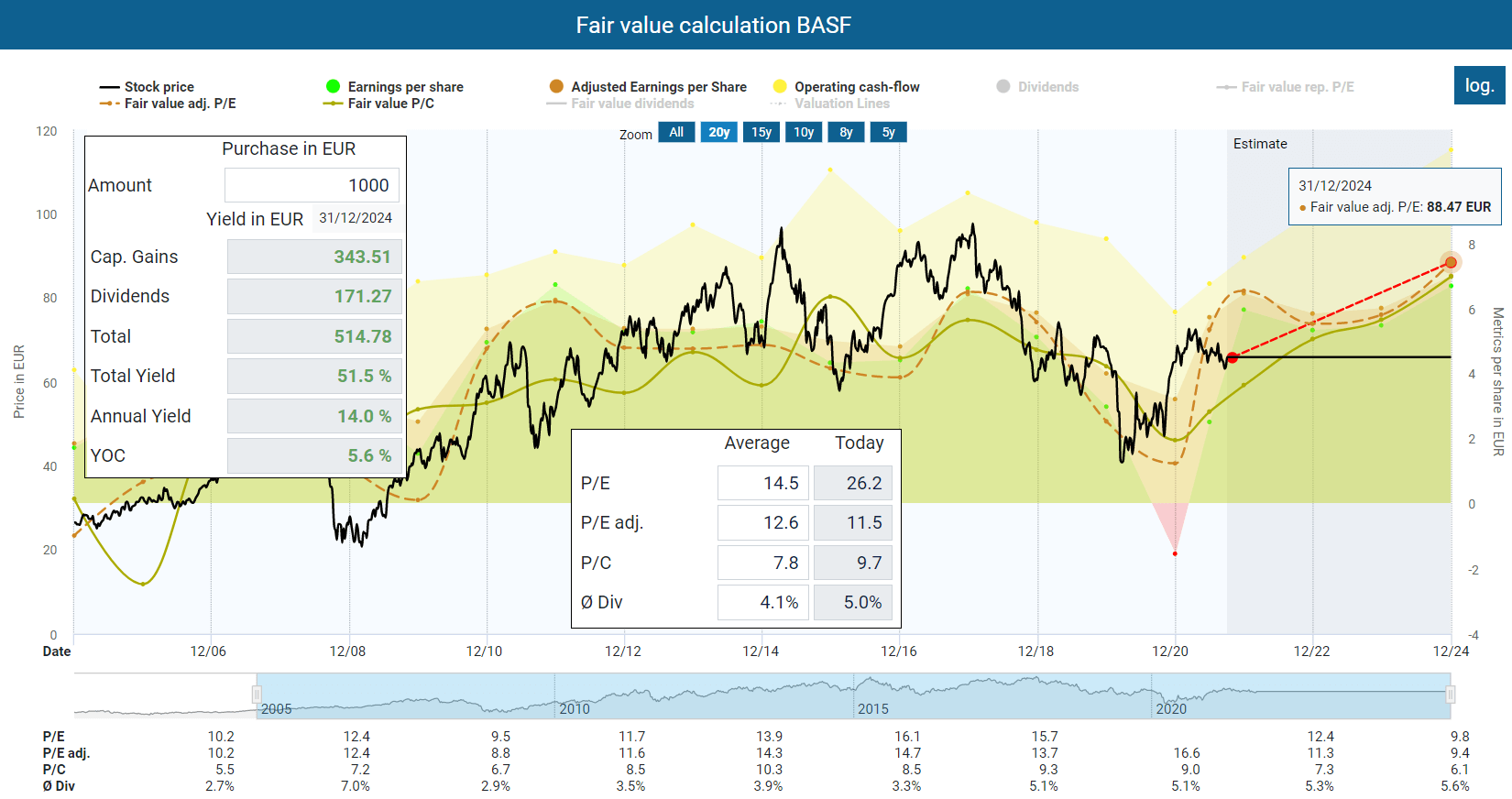

With the recent volatilities, some companies have become quite attractive again. This also includes BASF. At the height of the COVID-19 crash in March 2020, I was too hesitant and missed a good moment to enter. The share is currently consolidating. I have used the situation to take an entry and have built up a medium-sized position. The company has a solid balance sheet (debt ratio based on interest-bearing debts is only 23 percent) and a lovely dividend yield of 5 percent. The company also seems to be undervalued at the moment.

Why I bought my first

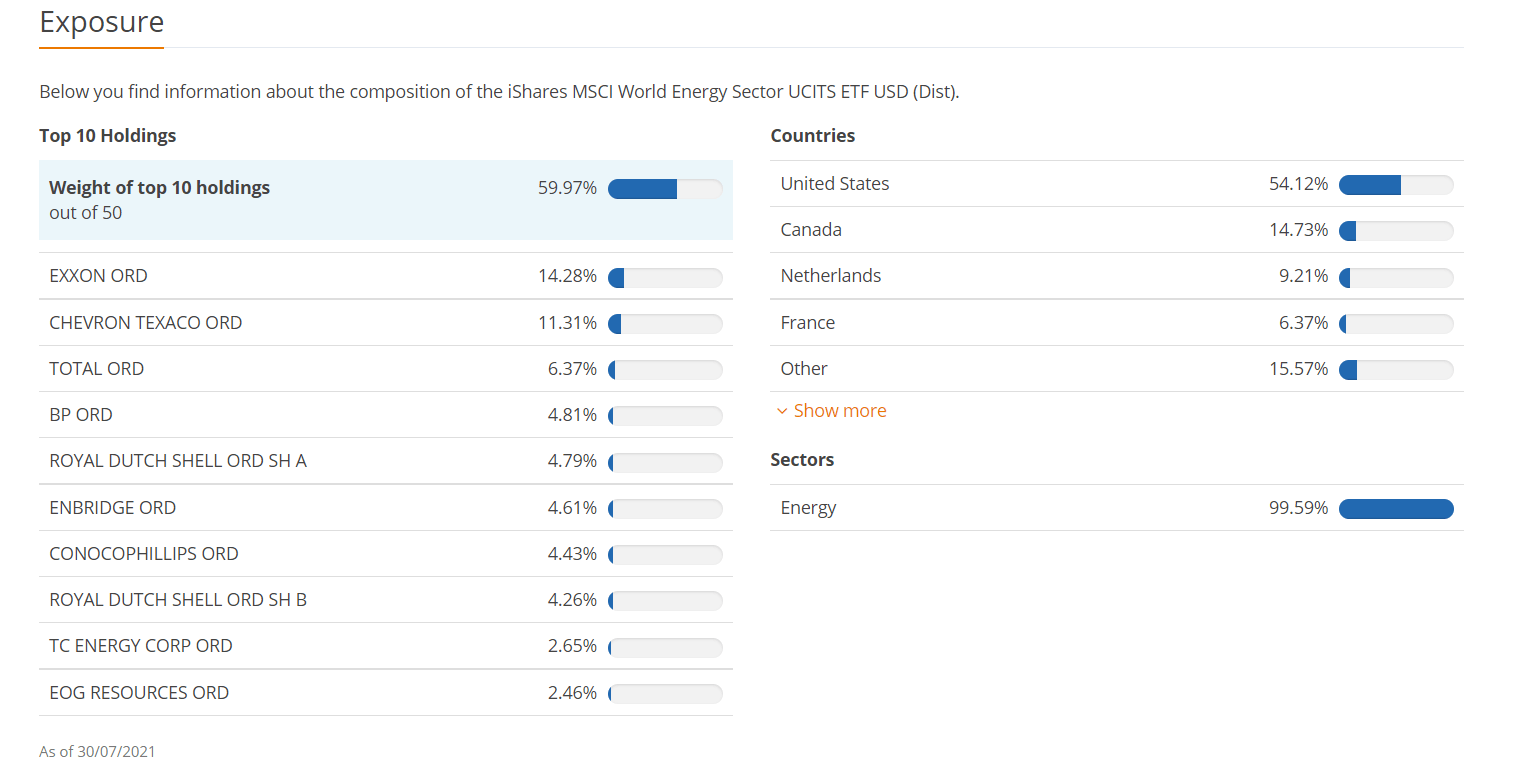

A slightly more significant move was my purchase of a new ETF. I opted for an iShares ETF that seeks to track the performance of an index composed of developed market equities in the energy sector. The reason for the purchase was the current development around the energy markets and the cheap valuation, and the high dividend yield of energy stocks. Although I already have Royal Dutch and Kinder Morgan in my portfolio, I still wanted to increase my share in energy companies. Depending on how the situation develops, I will sell my shares in Royal Dutch and Kinder Morgan and move the capital into the ETF.

So with this strategy, I’m following what I’m already doing with my Finance and Emerging Markets ETF. I bundle my investments in sectors that I have no idea about or where company performance depends on regulatory or unpredictable circumstances. When an industry is weakening, it is also more manageable for me to make follow-up purchases in many companies.

In total, the ETF holds 51 companies. The ETF’s most significant holdings are well-known old dinosaurs of the energy industry.

The dividend yield is around 4 percent, which is quite a considerable value that goes hand in hand with diversification.

I have also increased my existing holding in 3M. From my point of view, the company is simply a solid investment case. Sure, the growth of the business and the share price has been less than satisfactory. The company is also struggling with some lawsuits.

Regarding the lawsuits, I have a straightforward approach. Injustice should be punished and victims compensated. Judges decide on this, and I am prepared to bear the result as the company owner (the responsible management should nevertheless be sanctioned).

Accordingly, I am only looking at the fundamentals for the time being, and things look pretty good there.

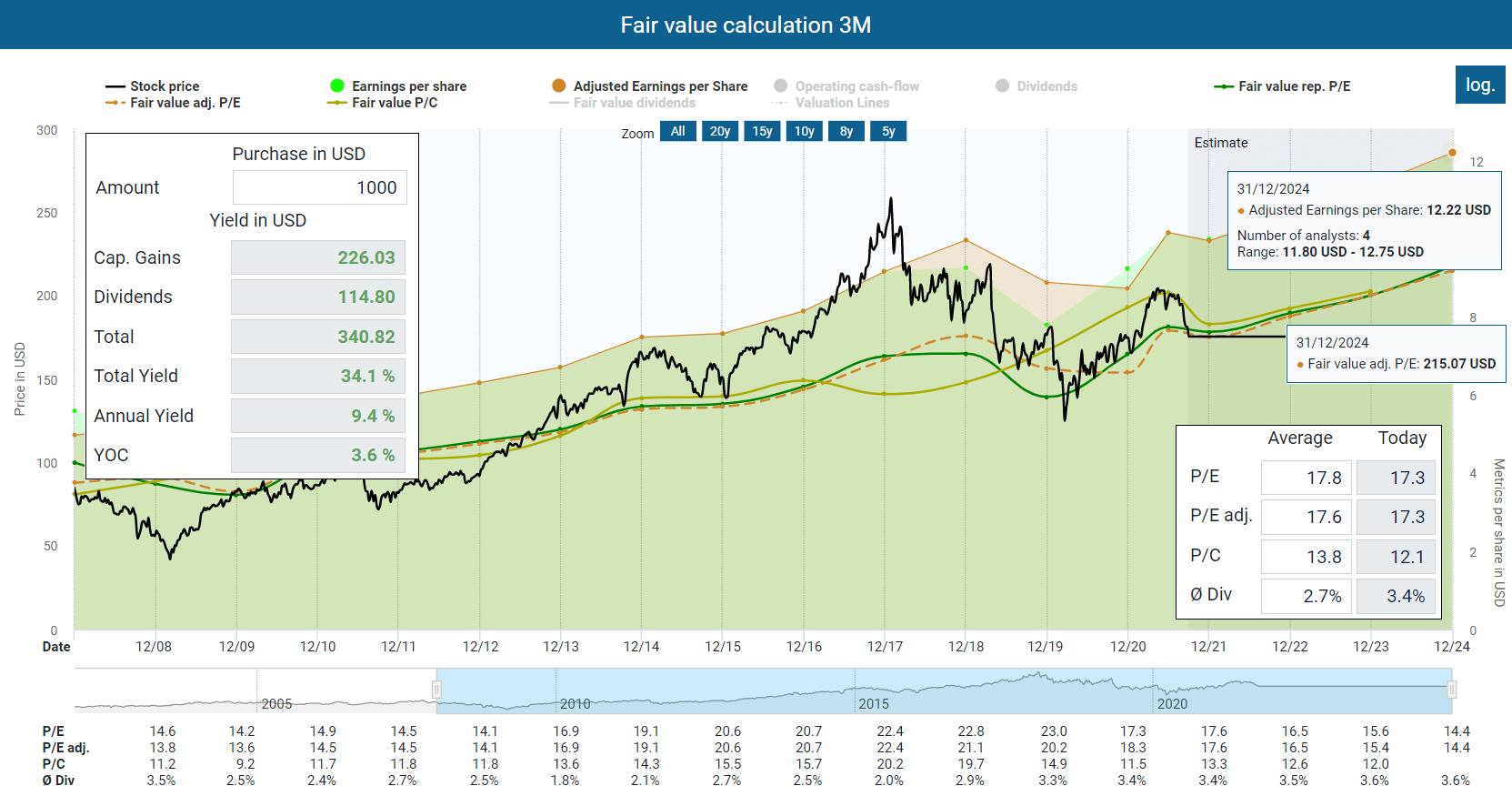

3M has made progress in reducing its debt. Interest-bearing debt was more than $21 billion in 2019. Today, it is only $19 billion. More than $3 billion of cash flow remains available after dividends. I like that. Turnover and profit are also expected to increase in the next few years, according to the analysts’ forecast. 4 analysts polled by FactSet Research report adjusted EPS between $11.80 and $12.75 for 2024. The forecasts are therefore not that far apart. If we assume that EPS rises from the expected $10 for this year to $12.22 in 2024, this results in an annual upside potential of the fair value of more than 9 percent.

In addition, the current dividend yield is historically quite high at 3.4 percent. The payout ratio of below 60 percent measured by cash flow and profit is also solid. At this valuation level, I will definitely continue to add shares of 3M to my portfolio.

Watchlist for October

There will be some additional share purchases next month. As you may know, I am relatively flexible when it comes to new investments. Either I buy new positions, or I increase my shares in existing investments.

The following companies are on my watchlist in particular:

- Microsoft (MSFT)

- Digital Turbine (APPS)

- Merck & Co. (MRK)

- Emerging Markets/Energy stocks

- Unilever (UL)

- General Mills (GIS)

If you look at my report from last month, you will likely see that none of the companies I bought were on my watchlist. Why is that? Is the watchlist nonsense, and in the end, I only do what I want anyway? Yeah, a little bit. I don’t have a fixed system for my stock purchases, and that’s one thing I have to consider changing.

However, I have an extensive overview of many companies that I look at from time to time. The watchlist contains primarily companies that I have examined particularly carefully, where substantial changes are imminent or companies that are in my focus for other reasons.

These companies are present to me in some form, which is why I put them on the list and perhaps monitor them a little more closely than other companies. But it often happens that I invest in different companies when it seems convenient at that moment.