I welcome you to a new episode of my Dividend Diary on the TEV Blog. Is there anything better in the financial world than a dividend income? Well, I guess not. And so, in December, I was again pleased to see a substantial increase in my dividends. I also used this month to add more shares and stocks to my portfolio. As always, in my monthly reports, I will give an update on my purchases. I document my monthly dividend income and the changes in my broadly diversified retirement portfolio. Here, I show you which companies have generated juicy cash flow for me each month and which stocks went into my basket. Besides, I analyze how the month has performed compared to the previous year. In the best case, my dividend income has increased.

As you know, I take care of my wealth management. To keep things simple, I have built three pillars:

- Active income.

- Passive income.

- Conversion.

Dividends fall into the last two categories. They are passive because I no longer have to work to receive the payments. Furthermore, they also contribute to the conversion because I reinvest the dividends and thus increase my passive income through dividends for the future.

My monthly dividend income in December:

This month I have received payments from the following companies:

- Johnson & Johnson (6.16 EUR)

- Archer Daniels Midland Co. (10.36 EUR)

- IBM (14.98 EUR)

- Snap-on (6.04 EUR)

- 3M (8.11 EUR)

- Royal Dutch Shell (6.50 EUR)

- Realty Income (2.98 EUR)

- Qualcomm (8.72 EUR)

- Kontoor Brands (4.87 EUR)

- V.F. Corp (10.09 EUR)

- Broadcom (10.91 EUR)

- Imperial Brands (9.72 EUR).

The total dividend income in December (after taxes) was: EUR 99.44/appr. USD 122.21

Dividend income check

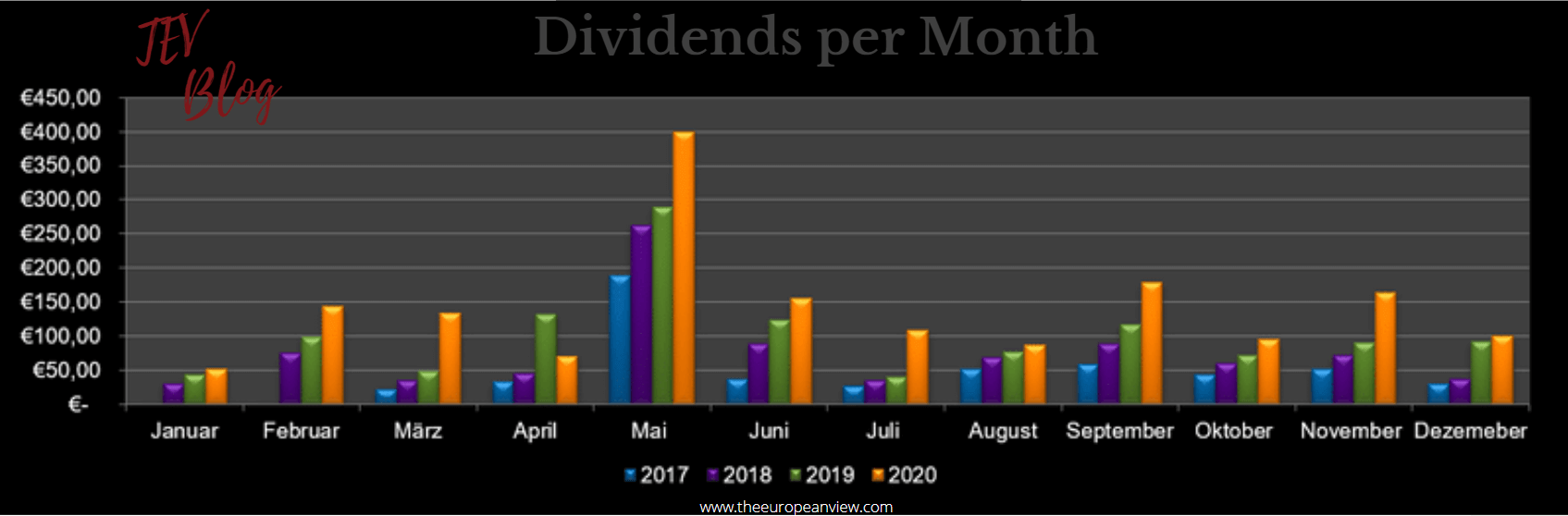

Now let’s see how the performance was compared to the previous year. Last year, I received only EUR 90,96 in dividends in December, which represents an increase of almost 10 percent. The comparability suffers somewhat because the December 2019 dividends are pre-tax. For 2020, however, my broker has already automatically deducted the taxes, so this year’s December figures are already after taxes.

Overall, I have received almost EUR 1,700 (after taxes) this year. That is far above the total dividend income of last year, which was slightly more than EUR 1,200 (before taxes). The overall development of my dividend income throughout the years is as follows:

Stock purchases for more dividend income

In December, I bought more shares of great companies so that the dividends will continue to rise in the future:

- AT&T (12 shares)

- Amundi Index MSCI Emerging Markets UCITS ETF DR (D) (7 shares)

- Snap-on (4 shares)

- 3M (4 shares).

In the following, I will briefly explain why I bought these companies. Please do not expect a fundamental analysis. I will only mention some aspects per company that might be of interest to the readers. Maybe you will find inspiration for your investment. In case you disagree, feel free to write your opinion about my purchases in the comments.

General thoughts

The year ended on a cheerful note in December. More or less, the stock markets continued the development from the beginning of the year and reached new all-time highs. So if you only look at the prices on January 1 and December 31, you could assume another successful year for investors. And even if this view is entirely correct, it only reflects the year’s reality in an incomplete way.

With the coronavirus, a black swan swept over the stock markets. People had to stay at home, were not allowed to work in their offices, and government bailouts had to save companies from going bankrupt. In such a crisis, people and families’ health and well-being take absolute priority over other aspects, which is why I am glad that the virus and its consequences did not personally harm my family and me. Therefore, the dividend income and the celebration of a higher passive income should only come in second (or even third) place.

But if we want to talk about financial things now, there are some lessons we can learn from the corona pandemic:

- Never, ever try to time the market.

- Enjoy the fact that stocks are passive investments.

- Buy, but pay attention to the value in return.

Never, ever try to time the market

Never, ever try to time the market. I have seen so many people who did not dare to buy stocks in February or early March. It was even worse for the investors who sold during this period, assuming that stocks would fall even further. I expect that we will see many more corrections and crashes in the future. But will the markets collapse again to such an extent that share prices will be below the prices of February and March? Who knows. But it’s a bet I don’t want to make.

Enjoy the fact that stocks are passive investments

Enjoy the fact that stocks are passive investments. Imagine you bought shares in January and then went on a world tour. You were on the ocean without the internet, and now you return home. There, you look at your depot. What will you see? Your capital will probably have increased. So it is worthwhile to ride out a storm. You don’t have to react to every development. For that, you have all the managers and CEOs of your companies, who are much more familiar with the circumstances and the company than you are.

I always buy more stocks, but I pay attention to the value in return

My approach is simple: I always buy more stocks, but I pay attention to what I get for my invested capital. I try to increase my ownership of great companies, especially during crashes. Nevertheless, I don’t buy everything that has a ticker.

From my perspective, you should always pay attention to the fundamental or intrinsic value of stocks when you make any investments. If you are not satisfied, don’t buy it. It is as simple as that. Often stocks come back to their average values. I wait for that moment and have a lot of patience. And when the time comes, I get greedy 🙂 . My investments in Leggett & Platt, Diageo, or Automatic Data Processing are good examples of this investment approach.

This month, my purchases were also driven by getting some value for the price tag, if possible, which is not so easy in the current market environment. Only the future will tell us whether my decisions were correct. Below you will find some brief explanations of my purchases.

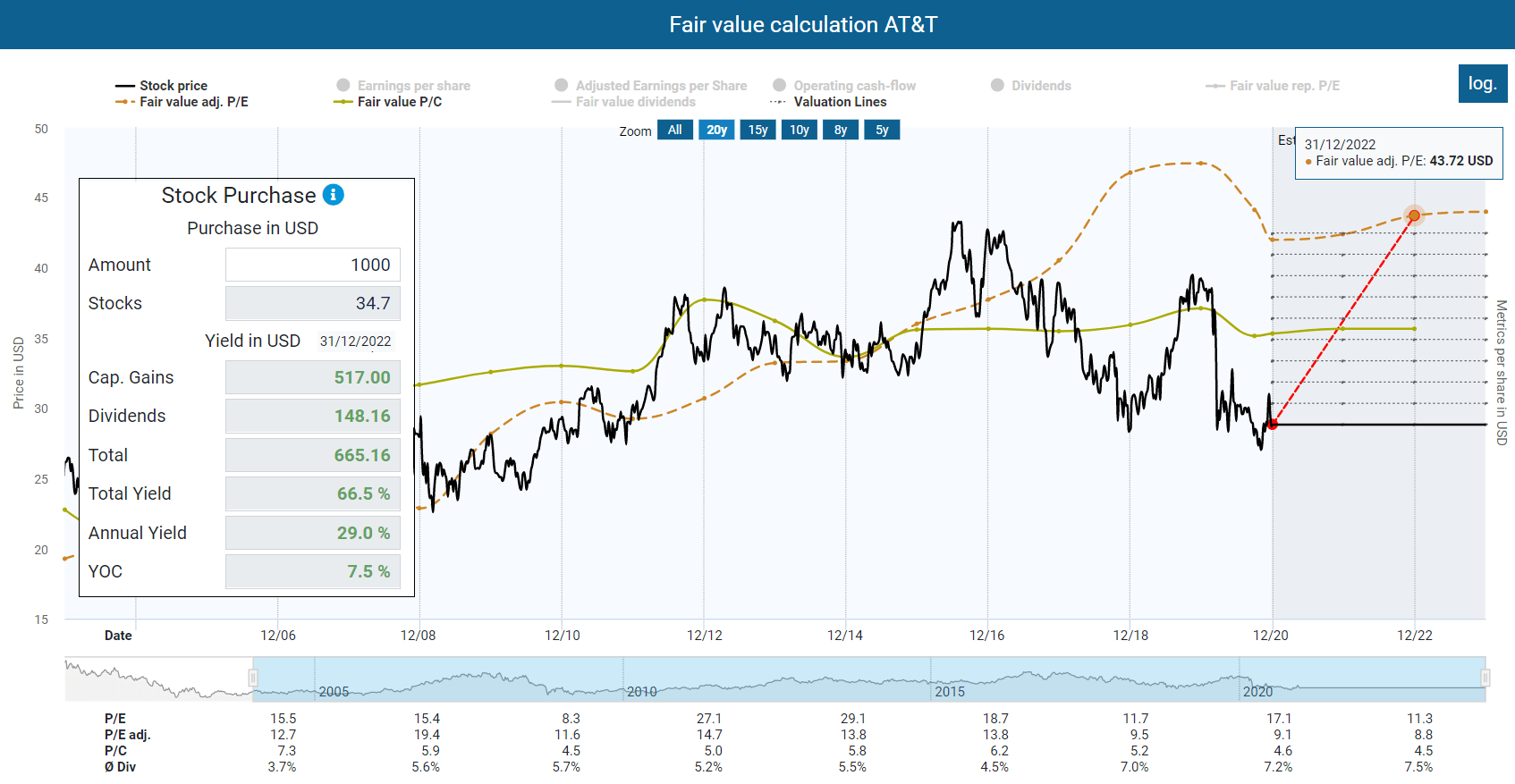

AT&T has been in my portfolio forever. At the same time, it is one of my worst stocks when I look at the stock price performance alone. Conversely, AT&T compensates shareholders with a reasonably high dividend yield, which currently stands at over 7 percent.

In recent years, AT&T has always announced in December that it would increase its dividend by 2 percent. This year, however, the company has not announced an increase. Many investors were disappointed.

I don’t think it’s a bad thing if AT&T keeps the dividend stable. Not increasing the dividend by 2 percent saves AT&T USD 300 million every quarter. Furthermore, the company will not lose its status as a dividend aristocrat yet, as long as it will increase the payout in 2021. I’m just patient and see what happens.

As you can see, the share price decline has pushed the stock deep into undervaluation.

The reasons for this underperformance are mainly AT&T’s debts, the poor execution of AT&T’s streaming plans, and the desperate need to generate a cash flow that is sufficient to address the expensive dividends and debt repayments. I raised all the points that bother me in more detail in an exclusive article on Seeking Alpha.

However, my critical stance should not obscure the fact that I see good opportunities for AT&T in the long term. The company is a cash flow machine and has an incredible treasure trove of assets in Warner Media. Furthermore, the mission to pay down debts reduction has been a pure success so far:

So far this year, we have refinanced more than 60 billion of debt at historically low rates, with about 30 billion of debt coming due through 2025. This has lowered our near-term debt maturities giving us ample financial flexibility in the years ahead. We now expect free cash flow of 26 billion or higher with a full year dividend payout ratio percentage in the high 50s.

In fact, we’ve reduced net debt by more than 30 billion since we closed our Time Warner acquisition a little more than two years ago. We continue to be active in the debt market. With interest rates at historical lows, we have been aggressive in refinancing our debt maturities and lowering our coupon rate.

We have reduced debt maturities by almost 50% over the next five years. This has extended our average debt maturity, which is a good place to be with rates as low.

In fact, we have lowered our average interest rate on debt to just under 4.1% with the lowest coupon rates we’ve ever seen. That gives us financial flexibility, not just for today but going forward as well. In fact, we ended the quarter with nearly $10 billion in cash on our balance sheet.

I have therefore bought a few new shares and am taking advantage of the cost average effect. So overall, I would never make AT&T my largest holding, but it is not a bad investment from my point of view.

Furthermore, I bought four more shares of Snap-on. The company has been in my portfolio since October. Back then, I purchased my first tranche in the company (8 shares).

As I wrote in my October report (click here to read the October report), Snap-on is a company that mainly produces and sells tools for professional applications, for instance, in the automotive and aerospace industries.

Snap-on’s product lines include hand tools, power tools, automotive diagnostics, shop equipment, tool storage products, automotive diagnostics software, other transportation services, industrial, government, education, agricultural solutions, and other commercial applications, including construction and electrical.

In November, Snap-on continued the trend of previous years by increasing its dividend by almost 14 percent. Added to this is a low payout ratio. Snap-on distributes only 37 percent of its profit and 31 percent of its cash flow for dividend payments.

The company is a solid investment for me. It will not grow tenfold in the next few years, but it pays a stable and growing dividend. According to my understanding of proper wealth management, Snap-on is a decent investment, which is currently not expensively valued.

3M has also been in my portfolio for some time. As with AT&T, I have bought tranches here from time to time. In December, I also treated myself to 4 more shares. From my point of view, the latest results of the company were quite convincing. I could well imagine that revenue and earnings growth could pick up again in the coming quarters. Maybe it will take longer. Who knows. In any case, I’ll stay invested and enjoy the rising dividends until then.

The Amundi Index MSCI Emerging Markets UCITS ETF DR (D) is my second ETF. My other ETF tracks the MSCI USA Financials Index (I wrote about it here). You can find a more detailed description of the Amundi Emerging Markets ETF here.

Watchlist for January

Next month, there will be some additional purchases of shares. I am relatively flexible here. Either I buy new positions, or I increase my shares in existing investments.

The following companies are on my watchlist in particular:

- Microsoft (MSFT)

- Merck & Companies (MRK)

- Intel (INTC)

- Salesforce (CRM)

- Mayr-Melnhof Karton AG

- Bayer

- Hugo Boss

- Sysco (SYY)

- AT&T (T)

If you look at my report from last month, you will see that none of the companies I bought were on my watchlist. Why is that? Is the watchlist nonsense, and in the end, I only do what I want anyway? Yeah, a little bit. I don’t have a fixed system for my stock purchases, and that’s one thing I have to consider changing.

However, I have an extensive overview of many companies that I look at from time to time. The watchlist companies are mostly companies that I have currently examined particularly carefully, where substantial changes are imminent or which are in my focus for other reasons.

They are present to me in some form, which is why I put them on the list and perhaps monitor them a little more closely than other companies. But it often happens that I invest in other companies, after all. And so it happens that I buy other companies because it seems convenient at that moment.

Have you received dividends this month? What’s on your watchlist? Let me know and write it in the comments.

Did you like the article? Stay tuned for the following content… It is all entirely for free! Enjoy!

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.