Welcome to a new episode of my Dividend Diary on the TEV Blog. Here, I report the development of a cash flow-oriented investment approach that focuses on generating a passive income through dividends. Against this background, the goal is not to outperform the market but to put food on the table through a regular income via dividends.

With the Dividend Diary, I document how a cash-flow investment approach can be part of well-balanced wealth management. To keep things simple, I have built three pillars:

- Active income.

- Passive income.

- Conversion.

Dividends fall into the last two categories. They are passive because they provide a cash flow without me having to go to work. Additionally, they are an essential pillar for the conversion since they can be reinvested to generate even more income in the future. That is the Theory. Now let’s get down to practice.

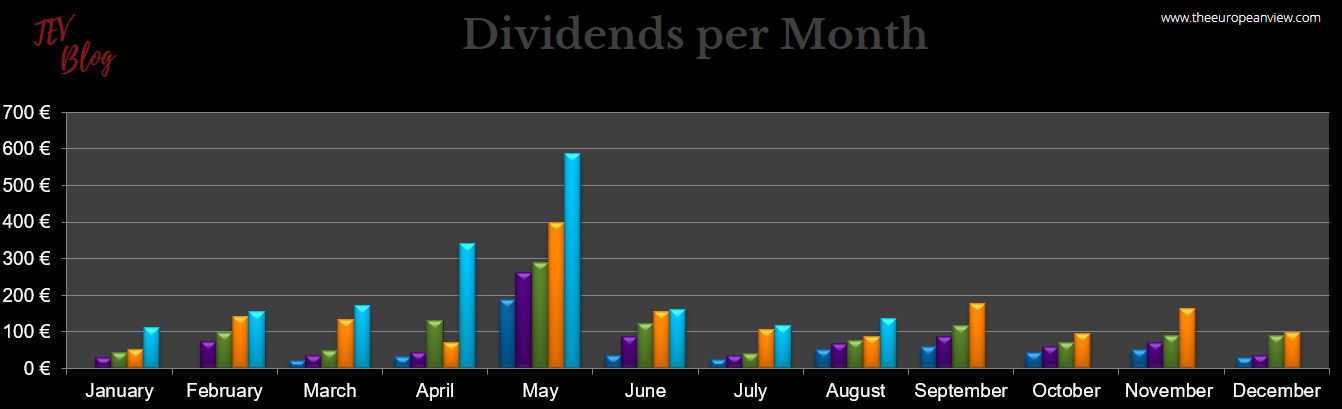

My monthly dividend income in August:

This month, my cash-flow approach generated the following income through dividends:

- Bristol-Myers Squibb (7.65 EUR)

- General Mills (20.08 EUR)

- CVS Health (5.61 EUR)

- AT&T (25.65 EUR)

- General Dynamics (5.96 EUR)

- Apple (7.78 EUR)

- Realty Income (3.14 EUR)

- Omega Healthcare REIT (9.32 EUR)

- Kinder Morgan (11.43 EUR)

- Procter & Gamble (12.08 EUR)

- AbbVie (21.33 EUR)

- Novo Nordisk (6.45 EUR).

The total dividend income in August (after taxes) was: EUR 136.48/appr. 160.53 USD

Dividend income check

August was another very successful month. After June’21 and July ’21, in which the dividend portfolio hardly brought any cash flow increases, August ’21 saw a plus of almost 60 percent compared to last year. With this growth rate, my monthly cash flow would more than double every two years. Thanks to my still high investment rate, I think this goal is realistic for the next few years. The overall development looks like this:

In the coming months, I expect to continue to exceed the previous year’s figures. The high increase in the value of the EUR last year should no longer have a distorting effect. In addition, my investments will surely provide one or the other cash flow increase.

Stocks I sold in August

I sold no shares this month.

Stock purchases in August

In August, I bought more shares of great companies so that the dividends will continue to rise in the future. All purchases were expansions of existing holdings. So no new companies entered my portfolio.

- Emerging Markets ETF (19 shares)

- Reckitt Benckiser (15 shares)

- Leggett & Platt (25 shares)

- Bristol-Myers Squibb (32 shares)

In the following, I will briefly explain why I bought these companies. Please do not expect a fundamental analysis. I will only mention some aspects per company that might be of interest to the readers. Maybe you will find inspiration for your investment. In case you disagree, feel free to write your opinion about my purchases in the comments.

Please keep in mind that this is only a non-representative sample of my overall asset management.

The first thing I did in August was to increase my holdings in emerging market companies. For this, I used my existing Amundi ETF that distributes dividends in November. My last purchases were in September 2020, November 2020, December 2020, April 2021, and June 2021. It is also very likely that I will add another larger batch in September.

The reason is simple and lies in the current situations surrounding Chinese companies (and I know how absurd it is to speak of an emerging market in connection with China – but so be it). China is a country with a long-term plan, and it will not sacrifice the success of its businesses for regulatory reasons. Tencent, Alibaba, etc., are all companies that can hold a candle to the big western companies and competitors such as Alphabet, Apple, Facebook, and Co. The Chinese government will therefore not touch the strength of these companies.

Plus: It’s funny (and not very consistent) how many pessimists write off Europe and the US and see China as the new great all-dominant world power but are now pouring out of Chinese stocks en masse. In my opinion, the discussion is too emotional. Would I put all my capital into Chinese stocks? No. But 10-20 percent? Yes, well-diversified across many companies in many sectors, in any case.

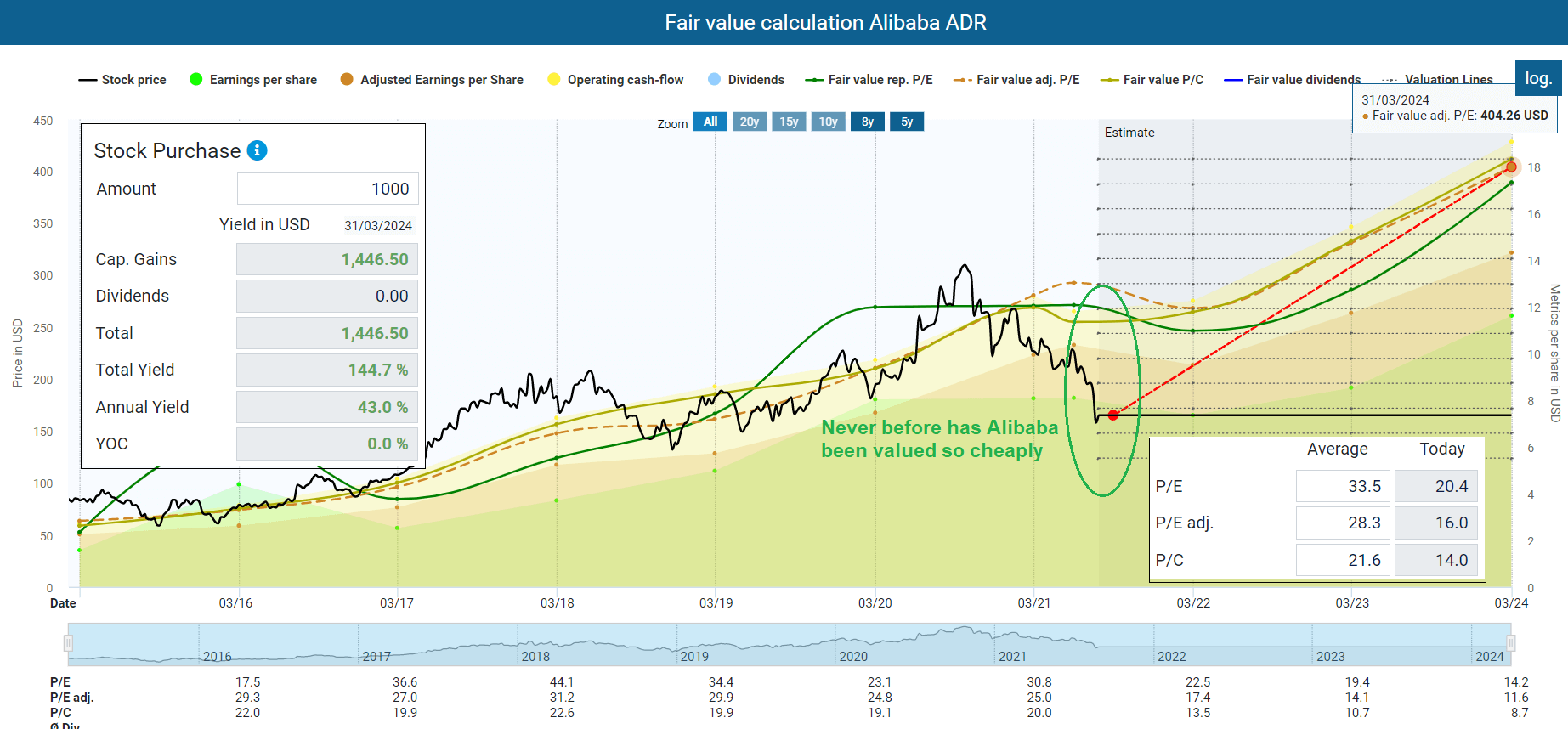

From a fundamental perspective, many Chinese shares are currently absolute bargains. Take a look at Alibaba. Its shares have never been as cheap as they are now. The company has an adjusted P/E ratio of just 16, which is crazy for such a growth company.

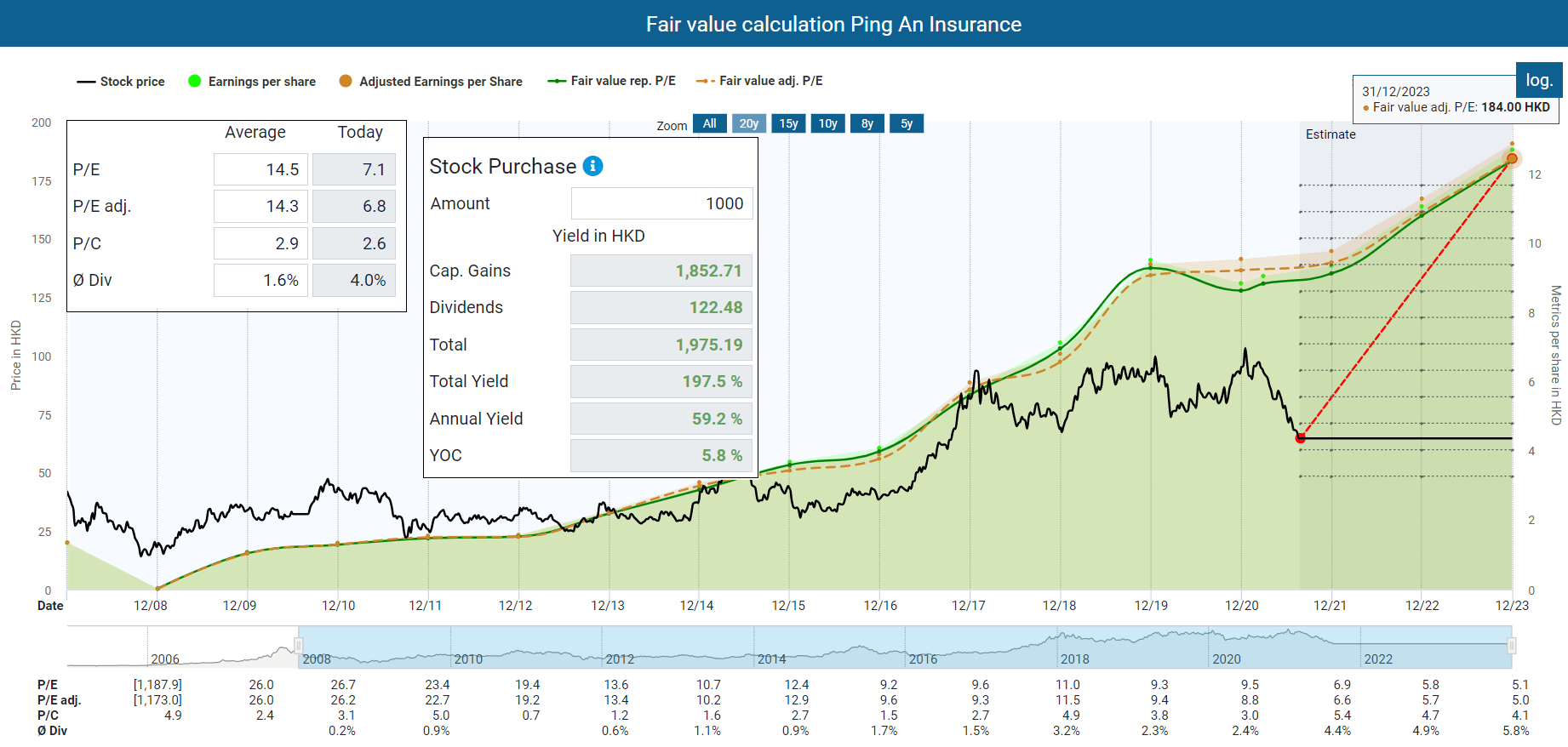

The same is true for other companies. Ping An Insurance is also well priced, plus it pays a respectable dividend of almost 4 percent. Nevertheless, the share price loses more and more and does not stop falling. At the moment I write this piece, Ping Insurance’s adjusted P/E ratio is only 6.8.

I could give many more examples like Tencent, Hengan International, or Chinese Mobile, etc. Everywhere we see the same picture. The shares have fallen massively even though the operating business is doing quite well.

The question is how investors should deal with this situation. I have sold my China holdings except for Ping An Insurance and moved the money into my ETF. The reason was this: it makes no difference which company I buy. The problem is not a company’s performance but how investors view Chinese companies and stocks in general. In other words, every Chinese stock carries the same “China discount” price tag.

In such a situation, I don’t want to bother with individual risks. I don’t want to bear fees for each purchase, etc. I just want to buy the whole market. In my view, emerging markets ETFs are an excellent opportunity to position oneself here for the long term. And that is what I am currently doing. By the way: The same considerations were decisive for my various purchases of additional shares in my US Financials ETF. So you can expect more investments of that kind in the coming months.

Reckitt Benckiser is one of my anchor holdings. Performance has been less good recently. However, I am interested in the long-term prospects.

Consumer goods companies have a unique appeal to me. They have strong brands (here, for example, Air Wick, Clearasil, and Calgon) for which demand exists worldwide. In addition, the companies act like holding companies. They can sell weak brands and buy strong ones.

I buy these companies when they are historically undervalued. This has worked very well for Procter & Gamble and, most recently, Danone. Based on this approach, I am currently increasing my investments in Kimberly Clark, Unilever, General Mills, and Reckitt Benckiser.

Following recent weak figures (inflation was a particular burden on Reckitt Benckiser in the last half-year), Reckitt Benckiser shares have fallen back to a fair valuation – enough to increase my holding. Based on the expected profits in the next few years, there is an upside potential of 30 percent (for 2024’s expected earnings per share).

The dividend yield is currently over 3 percent. Further increases are not necessarily likely for the time being, as Reckitt Benckiser first wants to reduce the payout ratio to 50 percent before new dividend hikes. For the full year of 2021, the payout ratio is expected to be somewhat around 60 percent.

Leggett & Platt has become something of a new darling in my portfolio. I like this relatively small company with a market capitalization of less than $7 billion.

The company has been on my watchlist for a long time. I finally bought it in the COVID-19 crash. The dividend yield there was more than 5 percent. Unfortunately, the position was not so big. Within a short time, the stock then rose by almost 100 percent, and I was on the verge of selling, as the parabolic rise had pushed the stock into overvaluation.

Since the overvaluation was not excessive, I held back. Fortunately, the stock is correcting (15 percent below the all-time high), which allowed me to add further shares to my existing holding. I would have preferred to wait for a more extensive correction, but that’s the way it is now. The money has to go somewhere. Leggett & Platt is currently slightly undervalued again and still has upside potential in the long term. So what is there to wait for?

My purchase of Palantir shares has nothing to do with the cash flow approach. Nevertheless, I write about it here, because this is my blog and I can write about whatever I want 🙂

I have doubled my Palantir shares right after the publication of the latest quarterly figures. Revenue increased by 50 percent and Palantir also raised its forecast for the full year. In the long term, Palantir expects sales growth of over 30 percent per year until 2025. Plus, the company is on the verge of profitability.

But these are analyst’s expectations, especially regarding profitability, and we all know how wrong these can be. However, when exactly Palantir will become profitable is less important to me for now. Palantir is one of the very few companies in which I invest despite losses. Actually, it is the only one with really sustainable losses which were mostly due to Palantir’s excessive stock-based compensation for its employees. All my other small caps investments are more or less profitable.

My investment thesis here is different and not so much profit-orientated. I don’t look for quick profitability. I like the CEO, and I love his “I don’t give a shit about your short-term thinking opinion” attitude because guess what, my brain says the same when people are posting their “I made 20 percent gains last week with my AMC to the moon trade” on Twitter.

Alex Karp, Palantir’s CEO, is brilliant. He has worked in many countries and experienced different work cultures. I also like the fact that he breaks away from the Silicon Valley mentality. Even if I don’t agree with everything he says, he is quite thought-provoking, and I like CEOs like him. The interview below with CNBC is excellent, and I have probably watched it three times. It shows pretty well Alex Karp’s thinking, ethic, and mentality.

The pharmaceutical sector was somewhat underrepresented in my portfolio for a long time. Apart from GlaxoSmithKline and AbbVie, I had no pharmaceutical companies in my portfolio for many years.

Then last year, I started to increase my holdings in this sector. I now have a prominent position in Johnson & Johnson, Pfizer, Merck & Co., and Bristol-Myers Squibb. Here, I am attracted by the comparatively fair fundamental valuation and the dividend payouts. So I’m gradually increasing my holdings in these companies.

At Bristol-Myers Squibb, the market also seems to recognize the potential. However, the company is still strongly undervalued. In addition, the balance sheet also looks somewhat better again. The debt ratio measured in terms of interest-bearing debt, for example, fell from 35.71 percent last year to the current 33 percent. I like the trend and expect more improvements in the future.

Watchlist for September

There will be some additional share purchases next month. As you may know, I am relatively flexible when it comes to new investments. Either I buy new positions, or I increase my shares in existing investments.

The following companies are on my watchlist in particular:

- Microsoft (MSFT)

- Digital Turbine (APPS)

- Merck & Co. (MRK)

- Emerging Markets

- Unilever (UL)

- General Mills (GIS)

If you look at my report from last month, you will likely see that none of the companies I bought were on my watchlist. Why is that? Is the watchlist nonsense, and in the end, I only do what I want anyway? Yeah, a little bit. I don’t have a fixed system for my stock purchases, and that’s one thing I have to consider changing.

However, I have an extensive overview of many companies that I look at from time to time. The watchlist contains primarily companies that I have examined particularly carefully, where substantial changes are imminent, or companies that are in my focus for other reasons.

These companies are present to me in some form, which is why I put them on the list and perhaps monitor them a little more closely than other companies. But it often happens that I invest in different companies when it seems convenient at that moment.