Welcome to a new episode of my Dividend Diary on the TEV Blog. Here, I report the development of a cash flow-oriented investment approach that focuses on generating a passive income through dividends. Against this background, the goal is not to outperform the market but to put food on the table through a regular income via dividends.

With the Dividend Diary, I document how a cash-flow investment approach can be part of well-balanced wealth management. To keep things simple, I have built three pillars:

- Active income.

- Passive income.

- Conversion.

Dividends fall into the last two categories. They are passive because they provide a cash flow without me having to go to work. Additionally, they are an essential pillar for the conversion since they can be reinvested to generate even more income in the future.

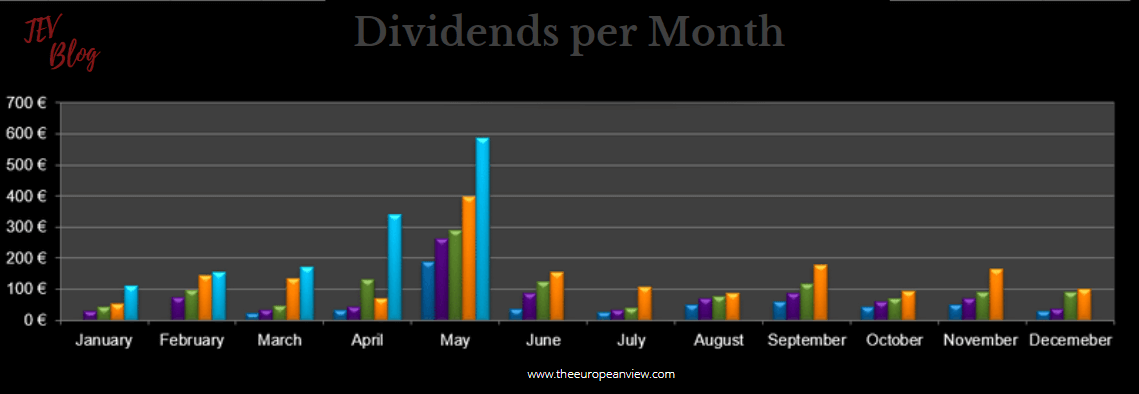

My monthly dividend income in May:

This month, my cash-flow approach generated the following income through dividends:

- AT&T (20.70 EUR)

- Munich Re (98.00 EUR)

- Danone (27.06 EUR)

- General Mills (16.39 EUR)

- CVS Health (6.29 EUR)

- Realty Income (3.02 EUR)

- Ab Inbev (3.85 EUR)

- General Dynamics (6.70 EUR)

- MSCI USA Financials UE 1D ETF (35.25 EUR)

- Allianz (124.80 EUR)

- Apple (8.58 EUR)

- Mayr-Melnhof Karton (23.20 EUR)

- AbbVie (22.87 EUR)

- Tanger Factory Outlet Centers (4.45 EUR)

- Hugo Boss (0.53 EUR) 🙂

- Kinder Morgan (11.11 EUR)

- Procter & Gamble (11.77 EUR)

- Omega Healthcare (9.07 EUR)

- Vonovia (76.05 EUR)

- China Mobile (21.24 EUR)

- Ping An Insurance (13.06 EUR)

- Fresenius Medical Care (19.73 EUR)

- Fresenius (22.68 EUR)

The total dividend income in May (after taxes) was: EUR 586.40/appr. 715 USD

Dividend income check

April was already a melt-up month, and sure, I appreciated the income hike. But seeing May topping April’s result by far shows that “more is always better”. The increase was also high compared with the previous year’s figure. In May 2020, I received “only” EUR 399 in dividends, almost 50 percent less than this year. Overall, the development over the last few years is as follows:

Stocks I sold in May

I also sold some shares in May:

- Archer-Daniels-Midland (12 shares)

- China Mobile (180 shares)

Below you will find a few reasons why I decided to sell these shares and why I sell stocks from time to time.

The last time I sold some shares was in February. Back then, I liquidated my entire Caterpillar holding. The holding was small and accounted only for an insignificant part of the overall portfolio. Based on its multiples, the stock was pretty overvalued. So I decided to take the profits off the table. I then used the freed-up capital to build up my first stake in Danone. The consumer goods company was valued much more favorably. Additionally, I could generate a higher cash flow from the invested capital (more details in my February Dividend Diary Report).

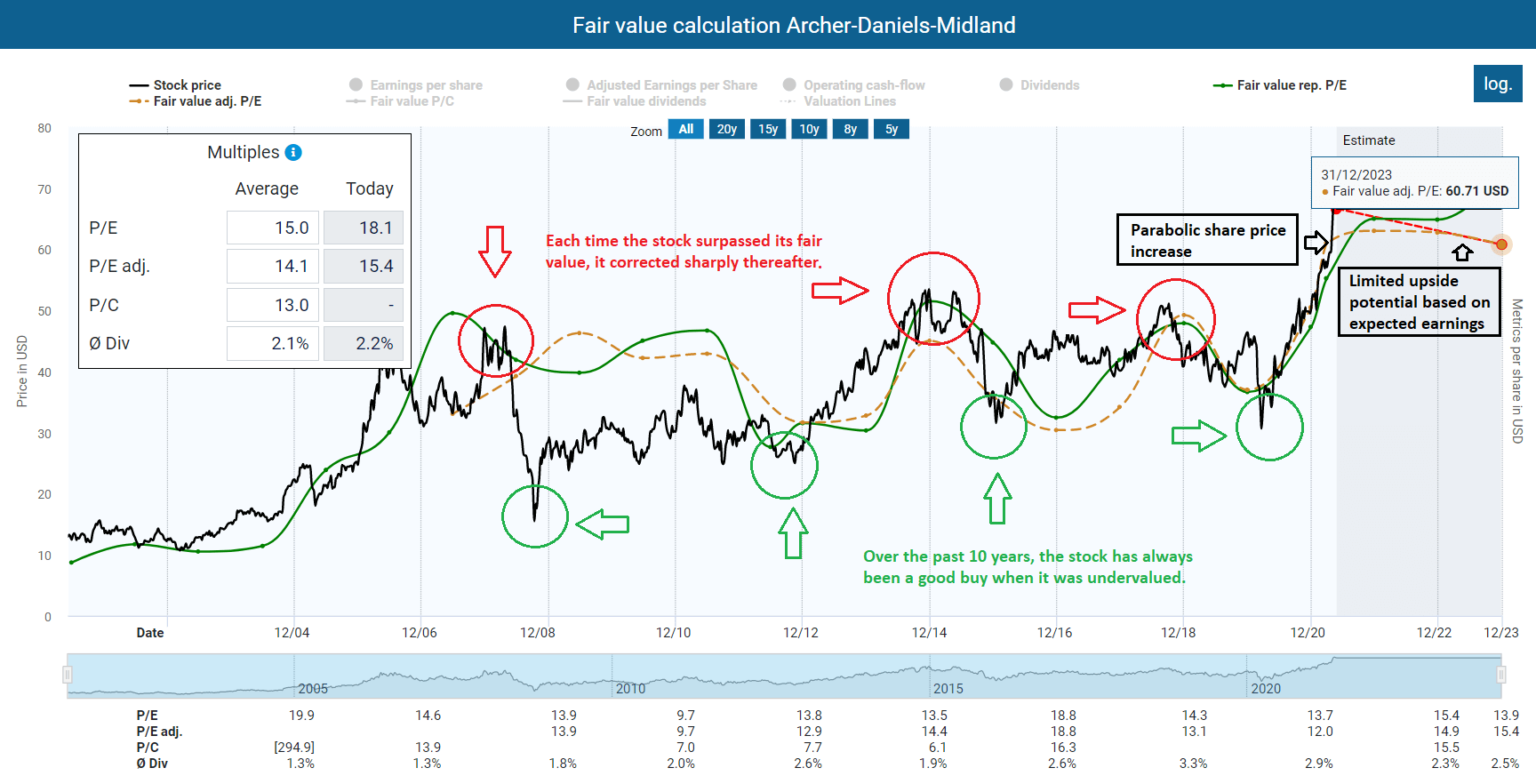

The sale of some of my Archer-Daniels-Midland shares followed the same logic. My last purchase of Archer-Daniels-Midland was not so long ago. Back in September 2020, I added 19 shares. But then and somewhat unexpected and due to a parabolic share price run, I had profits beyond 60 percent for this holding in my books. The rally had also pushed the stock far into overvaluation. So here I was again, facing another “Caterpillar situation”. That’s why I reduced my holding a bit. Now, I am still holding 35 shares in the company, which I will not touch further for the time being.

Why I liquidated my China Mobile holding

My investment in China Mobile was a one-off spontaneous action in January (see my January Dividend Diary Report). The stock was hit hard by the US sanctions, had a high dividend yield and a single-digit P/E ratio. Back then, I wrote:

I have absolutely taken my risk compliance into account here and only invested a minimal amount. Unlike with the other companies, I am not planning any subsequent purchases. The sanctions have no impact on China Mobile’s business. It is the same as it was a few years ago, only much cheaper. So the China Mobile purchase was a one-shot opportunity, and it is open to me how I will deal with the shares in the future. If the stock rises significantly in the next few months, I would also consider selling.

Well, and that’s what has happened now. I took the dividend in May, sold my holding at a low double-digit profit, and said farewell.

The stock is currently in no-man’s land. And yes, no one has ever died from bringing home a quick return of over 10 percent after just a few months. Lucky me, I guess. In addition, I had an exit strategy in place from the beginning (at least to a certain degree), which I have now realized. So, whatever happens to China Mobile, I’m at peace with it.

If there were a song about selling China Mobile, it would be the following:

Uhweee… I sold shares. Again… Let me shed some light on that.

While I would describe myself as a buy&hold investor, I still dare to sell some shares here and then. From my point of view, investing consists of risk and opportunity. For me, as a cash flow-oriented investor, the opportunity always lies in the potential cash flow, (almost) never in the potential book profits. So I always get curious when I can make a cash flow trade that is favorable to me. My “Caterpillar situation” back in February 2021 describes it best:

There I was. I had book profits of almost 50 percent. The capital tied up in the overvalued Caterpillar stock generated a historically low dividend yield of just 2 percent. My yield on cost was higher, of course, but this refers only to the initial capital and not to the total capital, including book profits.

Furthermore, risk and opportunity are closely linked. There are some bittersweet truths about investing that I accept and hold to. I wrote about them in a separate article (see here). Here, realities No. 3 and No. 4 are especially relevant. They are as follows:

- No. 3: Any further increase in the share price reduces the upside potential of a specific stock if there is no corresponding growth in the company’s underlying business at the same time.

- No. 4: Any further increase in the share price without an equivalent growth of the company’s underlying business increases my risk.

I use the cash flow trades only to increase my cash flow while slightly reducing the downside risk of my total assets at the same time. Additionally, I never sell my holdings completely (Caterpillar and China Mobile were exceptions, Archer-Daniels-Midland the rule), but only withdraw some capital from the existing holdings to increase my cash flow with investments in other companies that have a better opportunity/risk profile based on their fundamentals. Another advantage is that I also diversify my portfolio automatically.

Don’t confuse this approach with a foolish attempt to out-perform the market. I am far beyond thinking whether that is possible (if you raised an eyebrow here, read reality #5). My actions reflect my thinking.

Firstly, I want cash flow that puts food on the table. Secondly, I know that I can’t time the market, and lastly, I assume that anything that flies higher than it has fuel will eventually come back down.

Stock purchases for more dividend income

So back to business as usual. Last month, I bought shares in five companies:

- Kimberly-Clark (8 shares)

- TeamViewer (15 shares)

- Bristol Myers Squibb (25 shares)

- Pfizer (40 shares)

- V.F. Corp (10 shares)

Below, I will briefly explain why I bought these companies. Please do not expect a fundamental analysis. I will only mention some aspects per company that might be of interest to the readers. Maybe you will find inspiration for your investment. In case you disagree, feel free to write your opinion about my purchases in the comments.

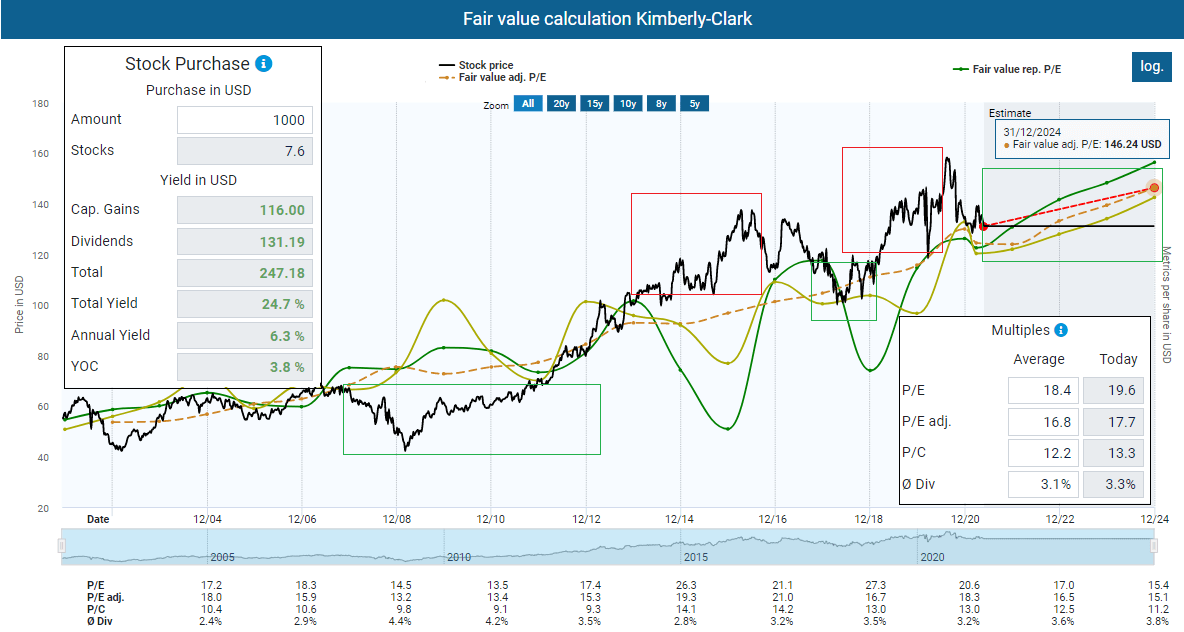

Relatively at the beginning of the month, I increased my existing holding in Kimberly-Clark. I am now sitting on 28 shares and am pleased with the dividend yield of over 3 percent. Kimberly-Clark is an anchor company in my retirement portfolio. I will therefore continue to expand the holding whenever good opportunities arise. If the stock decides to decouple from the steady operational growth to become an Archer-Daniels-Midland, I will make a cash flow trade. But I think that’s unlikely to happen for the time being.

The market was not so convinced by the quarterly results. Expectations are also somewhat mixed because the company is not expecting much for now. Neither do I, except for some cash per quarter. But overall, the company has always had phases in which the market was skeptical. In the long run, things worked out somehow.

I also bought more shares of TeamViewer. You got me. I did it. Again. And yes, I will continue to do so as long as I stay in line with my risk compliance and as long as TeamViewer delivers. The share has lost some momentum for no real operational reason. That’s just the way it is. The market is volatile. Apart from that, the Q1 results were quite solid and in line with what management had predicted. Billings increased by 26 percent, while growth in adjusted EBITDA came in at 22 percent. By the way, the gross margin remained at 93. That’s insane. Here is what I wrote in an analysis that I published on SeekingAlpha:

I took advantage of the dip and added more stocks to my broadly diversified retirement portfolio. I will continue to do so as long as I am convinced of my investment thesis. […] I’m not arguing that TeamViewer is a guarantee to wealth or anything like that. And yes, the valuation is still relatively high at the moment. But if you believe in the long-term growth prospects of the markets IoT, remote working, etc., you will find TeamViewer an excellent player with high profitability and good growth prospects.

Accordingly, I don’t need to elaborate on the investment thesis here, as TeamViewer is a permanent guest in the Dividend Diary. If you are interested, you can find more thoughts on TeamViewer in the November, August, February, and March reports.

At this point, I wanted to briefly justify why I think Pfizer and Bristol-Myers Squibb are good companies and good investment opportunities. But then I realized again how little I know about medicine, drugs, their approval, and whatnot. My limited knowledge is insufficient to give even a halfway valid reason without making a complete fool of myself in front of a more sophisticated person.

Management shall do their job

With these two companies, I simply trust management and the fact that both companies are historically fairly valued or even undervalued. They also have relatively high dividend yields and mature positions in a market that has a somewhat moderate valuation based on historical fundamentals.

Pfizer, in particular, has been on my extended watch list for some time. I like the dividend yield above 3 percent and think management knows what they are doing. Especially in the rush for a Corona vaccine, the company has proven that it can be flexible and achieve medical milestones quickly. Plus: The stock is not expensive based on historical fundamentals:

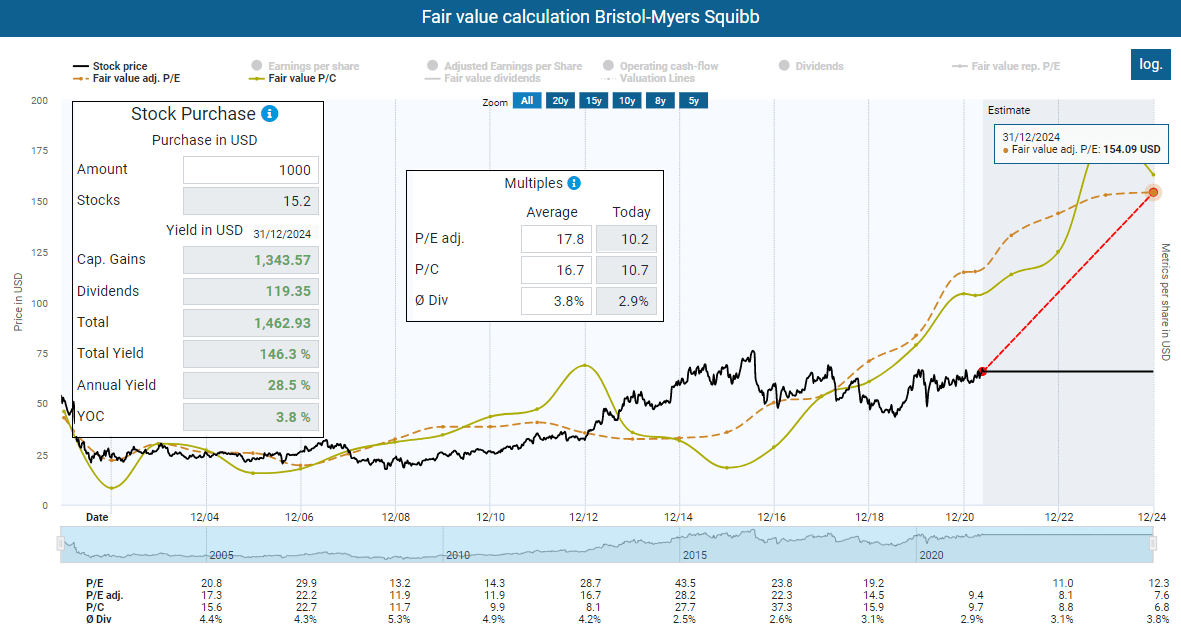

Bristol-Myers Squibb upside potential based on expected results and historical multiples is tempting

Compared to Pfizer, Bristol-Myers Squibb is valued even more favorably. Based on expected results and historical multiples, the annual upside potential is nearly 30 percent.

The debt ratio in terms of interest-bearing debt is “only” 33.85 percent, despite the $80 billion Celgene deal. In addition, Bristol-Myers Squibb sits on treasury shares worth $27 billion. Imagine what happens when the stock price goes up! Also, the cash mountain of more than $13 billion is a good sum compared to the interest-bearing debt of 50 billion.

It may bother one or two of you that I don’t delve deeper into the litigation problems that Bristol-Meyers faces and its merger with Celgene. But again, this is essentially about forecasting, which none of us can do, for a product market I don’t know enough about. I simply trust the management. The rest is proper risk allocation. So before I pretend to have mega insight here (analysts do that), I’ll just say that I’d like to be the owner of the company and expect management to do their job and leave me a piece of the profit pie.

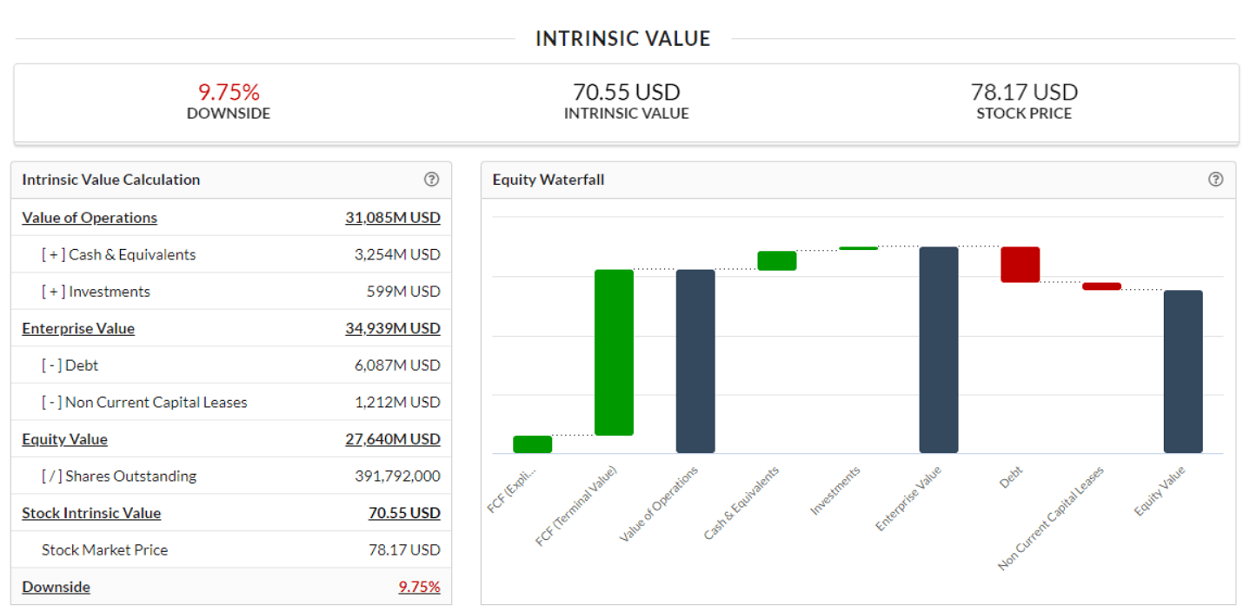

My last purchase in May was V.F. Corp. The company has been in my portfolio for a long time, and I am a big fan of the management. For me, V.F. Corp. is the Procter & Gamble of the apparel world. Both companies benefit from their size alone. They buy profitable brands and divest the lousy business. Such transformations can take time but usually succeed in the long run and open up good buying opportunities.

No question. V.F. Corporation is currently overvalued. Various valuation methods show that. Here you can see a calculation of the intrinsic value based on the discounted cash flow model.

Also, based on historical multiples, we see that there is not much to win at the moment. So fair enough, it is hard to justify the purchase as “absolutely necessary”.

But despite a somewhat higher valuation, the company has good momentum. The online business is booming, the Chinese market is growing excellently, and the acquired Supreme brand is delivering as hoped (the general plan is to increase Supreme’s sales by 8 to 10 percent per year). Here are some numbers, taking from an article I published on SeekingAlpha:

Revenue increased 23 percent to $2.6 billion in the latest fourth quarter. Organic growth amounted to 16 percent. Adjusted operating income increased organically by 59 percent, while adjusted EPS even doubled. All four strategic brands contributed to the growth. Vans grew 13 percent, The North Face grew 28 percent, Timberland grew 25 percent, and Dickies grew 22 percent. Highlights were organic growth of 65 percent in the DTC Digital business and nearly 100 percent in Mainland China.

Sure, there are base effects at work here since the quarter last year was affected by COVID-19, but my investment is long-term, and I know the risks and have my risk compliance in place. So everything is fine.

Watchlist for June

There will be some additional share purchases next month. As you may know, I am relatively flexible when it comes to new investments. Either I buy new positions, or I increase my shares in existing investments.

The following companies are on my watchlist in particular:

- Microsoft (MSFT)

- Digital Turbine (APPS)

- Intel (INTC)

- Salesforce (CRM)

- Mayr-Melnhof Karton AG

- SAP (SAP)

- Bayer

- Hugo Boss

If you look at my report from last month, you will likely see that none of the companies I bought were on my watchlist. Why is that? Is the watchlist nonsense, and in the end, I only do what I want anyway? Yeah, a little bit. I don’t have a fixed system for my stock purchases, and that’s one thing I have to consider changing.

However, I have an extensive overview of many companies that I look at from time to time. The watchlist companies are primarily companies that I have currently examined particularly carefully, where substantial changes are imminent or which are in my focus for other reasons.

These companies are present to me in some form, which is why I put them on the list and perhaps monitor them a little more closely than other companies. But it often happens that I invest in different companies when it seems convenient at that moment.

Besides Alpha Spread, I also find ValueInvesting.io and Finviz useful when trying to figure out whether a stock is undervalued.